This document is being provided for the exclusive use of blake@sandboxfp.com.

20 June 2024

The J.P. Morgan View

Unwinding carry trades

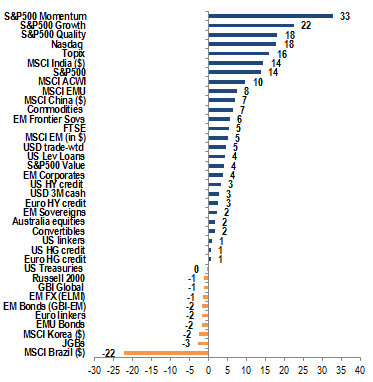

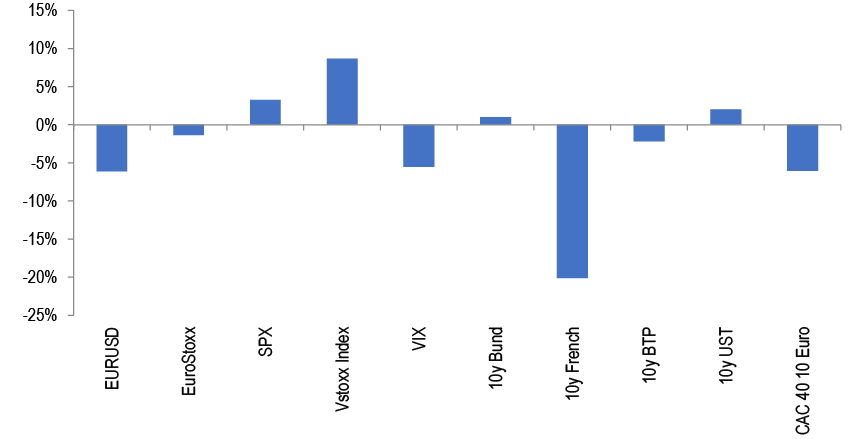

YTD returns by asset

Source: J.P. Morgan.

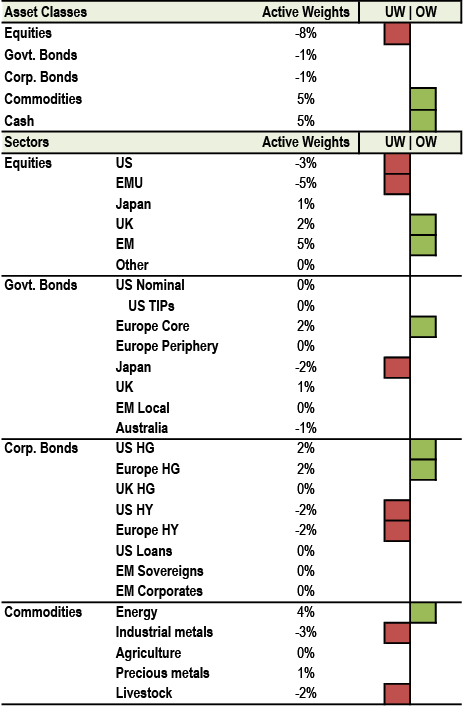

Cross-Asset Strategy: Bonds rallied amid softer US inflation data and flight-to-quality flows after the snap decision by French President Macron to call a Parliamentary election. Despite softer inflation data, Chair Powell struck a less dovish tone and the median dots suggested just one cut this year. With markets pricing in two cuts and yields at the lower end of their ranges, we turn tactically bearish 5Y USTs. While French spreads have started to price in a higher probability of tail risk scenarios, there are fiscal constraints to an NR government; we are neutral Euro duration and hold 5s/10s Germany. We see no change in BoE policy or guidance at this week’s MPC meeting, and remove our bullish duration bias on the rally in rates. The macro backdrop is supportive for US HG, but lower yields may be a near-term headwind to already tight spreads. US HY credit metrics show broad-based deterioration but remain historically strong. In FX, a rotation away from carry to other drivers of returns has been a key theme for us given expectations of yield compression that would make FX carry vulnerable to vol shocks. Brazil equities are cheap, but face headwinds from persistent outflows and high domestic opportunity cost from double-digit policy rates.

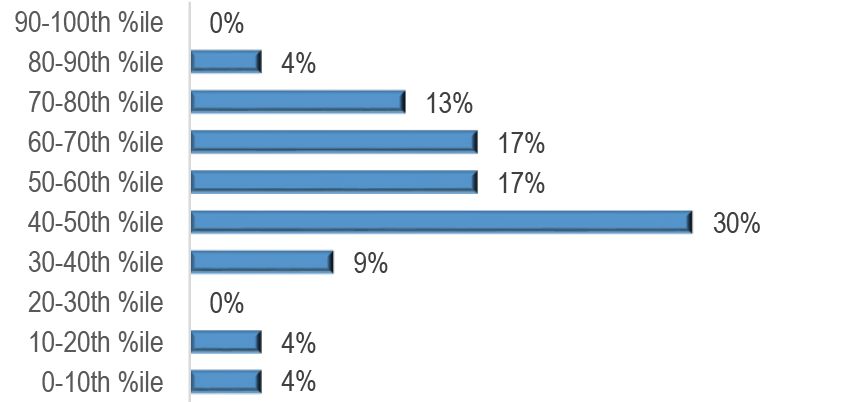

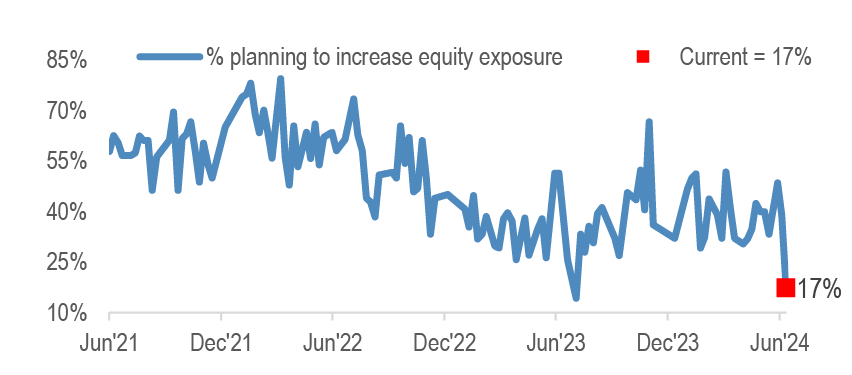

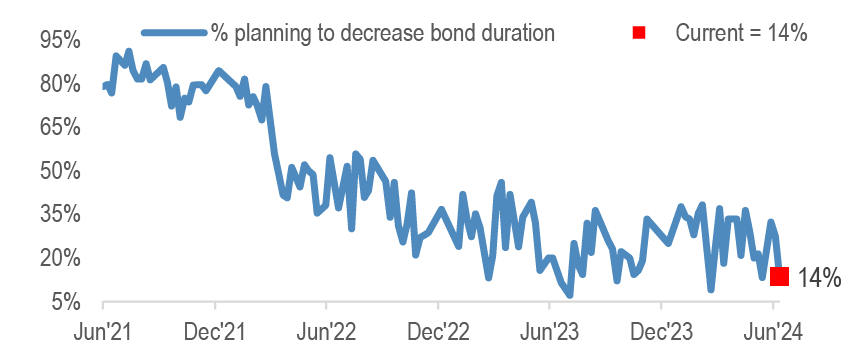

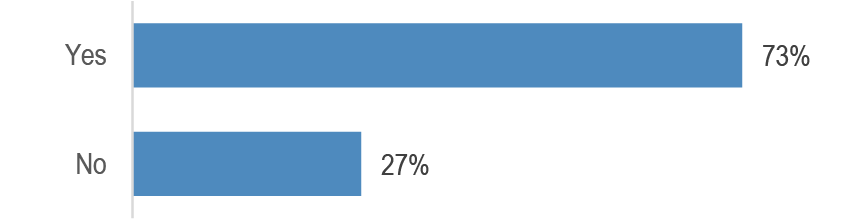

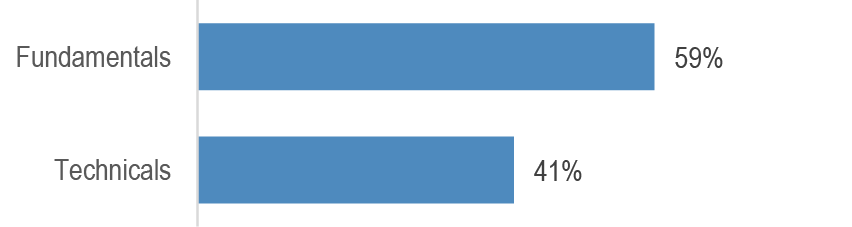

JPM Clients’ View: Click here to take this week’s survey . This week we poll investors on European elections, the Fed and CPI, in addition to our running sentiment questions. Our last survey results indicated: (1) average equity exposure/sentiment is ~52nd percentile; (2) 17% planned to increase equity exposure, and 86% to increase bond duration near term; (3) 61% believe markets haven't fully priced in recent EM elections and 73% believe they are underpricing risks around remaining elections this year; (4) 59% believe the recent decline in oil was primarily due to fundamentals; (5) respondents saw the June ECB meeting as modestly more hawkish than expected.

Long carry/short volatility trades are being unwound: Election surprises sparked an unwind of carry trades including the French-German yield spread, peripheral euro area sovereign spreads, and MXN. Political and liquidity risks continue to pose downside to crowded long carry/short vol trades, including US equities, which are at risk if political headwinds intensify into the US election. While the benign US CPI and PPI reports provide some relief, our bias is to view these inflation surprises as one-offs. The narrow path for a soft landing and very little recession risk priced into risky assets also pose downside risk if cycle worries were to return.

New trades:US / Euro credit trades for 2H (Doctor / Lamy); Euro Banks option trades (Silvestrini); Schatz call spreads (Gupta).

Cross-Asset Strategy

Economics

Inflation drop trumps Fed caution in market pricing of Fed. Chair Powell linked the change in this year’s dot plot to a lack of progress on lowering inflation this year. By contrast, US rates rallied last week and price a lower year-end policy rate than the latest Fed dot plot. The main catalyst for this move was a surprisingly low set of May inflation readings. The Fed has signalled it will remain patient in the face of modest inflation disappointment, but the market also recognizes that it will likely move toward easing relatively quickly if the May reports are followed by a string of moderate inflation readings.

France snap election and excessive deficit procedure is not a good mix. President Macron called snap lower house elections due to the rise in far-right support. Developments so far have been unfavorable for Macron as the Left formed an alliance, significantly raising the risk that Le Pen’s NR wins a majority in the lower house. There are signs that the NR has moderated some of its positions over time, but concerns around their stance on fiscal matters remain, particularly given France is about to enter an Excessive Deficit Procedure. An NR-led government could test the new EU fiscal framework, which could have far-reaching implications, a concern reflected in the OAT-Bund spread spiking to above 70bps.

South Africa GNU points to centrist rule; Mexico reforms a concern. After the recent EM elections, political and policy risks are shifting. Post-election uncertainty had appeared highest in S.Africa, but the GNU deal clears the way for Cyril Ramaphosa to be re-elected. In contrast, policy risk in Mexico has risen after Morena’s constitutional majority was confirmed. Of particular concern is the planned overhaul of the judiciary system, which would weaken the Supreme Court and eliminate the Injunction Law. A silver lining is the government’s ability to approve fiscal plans, but we expect only a watered-down, 2-step fiscal plan to be implemented over 2Y.

Equities

QTD Defensive sectors are trading in-line in Europe, a change from Q1 where they underperformed. We believe this shift will last, on further repricing of a range of tail risks, and reiterate our barbell of OW Defensives and Commodities. This is in contrast to the frequent feedback from investors that one should be buying Cyclicals now that PMIs are picking up. US growth momentum is slowing into year end, and bond yields are likely to be flat or move lower into year end, which should support bond proxies (Equity Strategy, Jun 16th).

Our cautious stance has been based on our view that there is no re-rating upside, and that any upside had to therefore come from earnings growth, which we see being insufficient to take on equity risk even under best case scenario assumptions. For equities to avoid a 20%+ correction, you have to believe that tech will become a much more meaningful driver of growth for the broad economy in short order. While we believe tech will continue to be the key driver of economic growth for years to come, we don’t think its impact on corporate P&Ls across the board will be that profound so suddenly, and so we remain cautious here, expecting economic growth to weaken, equities to correct, and investors to find a better entry point (The SMid View, Jun 11th).

June BoJ monetary policy meeting and implications for stock market. Following the dovish decision, the market could push out its outlook for the pace of interest rate growth, but we also see potential for a gradual easing of yen depreciation pressure, which has weighed on Japanese stocks. The BoJ plans to present a policy for starting JGB reductions on a “substantial scale” at the July MPM. We remain OW on financial and consumer spending-related stocks (Japan Equity Strategy, Jun 14th).

Brazil equities are cheap, with many quality stocks trading below 10x forward P/E and +10% EPS growth. Brazil is exposed to the global story: Fed easing, China stronger equity performance, stronger global PMIs are all potential positive catalysts. Yet, two main domestic obstacles remain to allow value perception to come to higher price reality: (1) persistent domestic outflows; and (2) high domestic opportunity cost from double-digit policy rates (EM Lighthouse, Jun 17th).

Bonds

Bonds rallied sharply amid softer US inflation data and flight-to-quality flows after the snap decision by French President Macron to call a Parliamentary election. Despite softer inflation data, Chair Powell struck a less dovish tone than in recent FOMC press conferences and the median dots suggested just one cut this year. With markets pricing in two cuts vs. one cut in our forecast, yields at the lower end of their ranges, last week’s moves amplified by flight-to-quality flows, and this week’s activity data expected to turn more positive, we turn tactically bearish 5Y USTs and keep 5s/30s steepeners.

In the Euro area, a flight-to-quality rally along with the softer US inflation data supported Germany. While French spreads have started to price in a higher probability of disruptive tail risk scenarios, there are fiscal constraints to a National Rally government. We are neutral duration and pare back on bullish exposure by taking profit on 1Y/1Yx1Y €STR curve flatteners. We hold 5s/10s Germany and 2Yx2Y/ 10Yx10Y EUR swaps steepeners. In the UK, we see no change in BoE policy or guidance at the MPC meeting. The rally in rates means we remove our bullish duration bias, and close 1Y/1Yx1Y SONIA curve flatteners.

In EM, a combination of local concerns over judicial independence in Mexico and fiscal policy in Brazil, as well as upcoming US elections that shorten the runway for tactical opportunities, we pare back on risk by turning neutral Brazil and Colombia local duration (Latam Local Markets, June 13th). We are neutral local duration overall, with OWs Poland, Türkiye and Uruguay offset by a short duration overlay and an UW in Thailand (EMOS, Jun 6th).

Credit

The macro backdrop is supportive, but lower yields may be a near-term headwind to already tight spreads. Key positives for US HG credit spreads include the strong equity markets rally, reasonable dealer positions, and a slowdown in supply. However, valuations are tight leaving limited room for further tightening, and the recent decline in yields poses a challenge. It remains uncertain whether it will cause some investors to step back. While the move down in yields last week is due to benign inflation data, which is a favorable driver, historically spreads struggle to tighten when yields are declining, until they stabilize again (CMOS, Jun 14th).

US HY credit metrics show broad-based deterioration but remain historically strong. A review of 1Q24 credit metrics unveiled erosion in credit metrics given 1) a q/q increase in leverage (though leverage remains comfortably below the long-term average), 2) EBITDA declining on a y/y basis for only the second time since 2020, 3) profit margins deteriorating to a 3Y low, and 4) interest coverage ratios dipping below 5x for the first time since 4Q21 following double-digit increases in LTM interest expense for four consecutive quarters (1Q24 High Yield Credit Fundamentals, Jun 12th).

At such rich valuations, the investment case for Euro credit rests on this ‘not too hot - not too cold’ environment holding while the disinflation process plays out. In our view, investors have become largely de-sensitized to headline noise after 4Y of history defining events, which means that volatility is likely to remain low provided that the economy remains broadly healthy. Technicals could strengthen further over 2H24 on slower supply, as there is only a short window for primary due to the sports and political calendar. European growth is recovering, supporting credit fundamentals and suppressing default rates. We revise our Euro IG spread forecast down slightly to 120bp, essentially flat to current levels, and look for a more moderate 55bp widening in Euro HY to 375bp (European Credit Mid-Year Outlook, Jun 12th). In our view, the French elections pose a tactical buying opportunity. However, we would focus on segments that have only been indirectly affected, such as Italian bank AT1, short-call corporate hybrids, or subordinated insurance. Following the outlook, we have added OW LL vs HY and OW B vs BB to our top trade portfolio (European Credit Weekly, Jun 14th).

Currencies

When yield compression and volatility collide. A rotation away from carry to other drivers of returns has been a key theme for us. The view was motivated by expectations of yield compression which would make FX carry vulnerable to any vol shocks. This staple source of currency returns for two years finally met its reckoning as a series of VaR shocks eliminated most of carry YTD returns. While certain high-yielders could recover depending on idiosyncratic developments, global FX carry remains vulnerable given lower yields; by contrast G10 carry is likely to be more resilient given sticky inflation. The sum total of US developments is that yields have peaked for now and by extension, that USD upside from higher yields is dissipating for now. The dollar is overshooting US yields, so can weaken in the near-term if vol subsides. But US elections will ultimately limit USD weakness.

G10 forecasts: EUR/USD 3Q 1.05 unched. Yen downgraded on BoJ; USD/JPY 4Q 156 (153). GBP upgraded on growth; EUR/GBP 0.83 (0.87). EM: CNY downgraded on Fed. USD/CNY 7.30 (7.25). USD/INR 83.80 (83.90). HUF, CZK upgraded. EUR/HUF 390 (400). EUR/CZK 25.75 (26.00). ZAR unchanged; shift to constructive bias. Latam downgraded. USD/MXN 17.75 (17.50). USD/BRL 5.20 (5.10) (KCV, Jun 14th).

Commodities

Acknowledging the notable slowdown in drilling activity, we reduce our 2024 US crude oil output estimates. While oil recovered per foot drilled in the US shale basins fell 12% since its peak in 2021, operational efficiencies, which began being implemented more widely last year, are more than offsetting declining productivity and relatively low rig count. On an annualized basis, we project another 400 kbd growth in US NGLs supply in 2024 and an additional 350 kbd in 2025 (Oil Markets Weekly, Jun 13th).

Major exporter grain stocks decline to critical lows in the otherwise benign June WASDE. Markets had arguably digested much of the fundamental adjustments embedded in the June report during 2H May; however, associated risk premiums have also since eroded across the wheat complex. We stay long the agri complex via an index as our price forecasts sit above futures curves, and markets are discounting supply-side and geopolitical risks – which remain heightened, in our view. Our highest-conviction long underlyings are ICE #11 Sugar, CBOT Wheat and CBOT Corn (Agricultural Markets Weekly, Jun 13th).

This week, we poll investors on European elections, the Fed and CPI, in addition to our running survey questions on equity positioning/sentiment, and intentions for near-term changes to equity allocation and bond duration. The results from the last survey are shown below.1

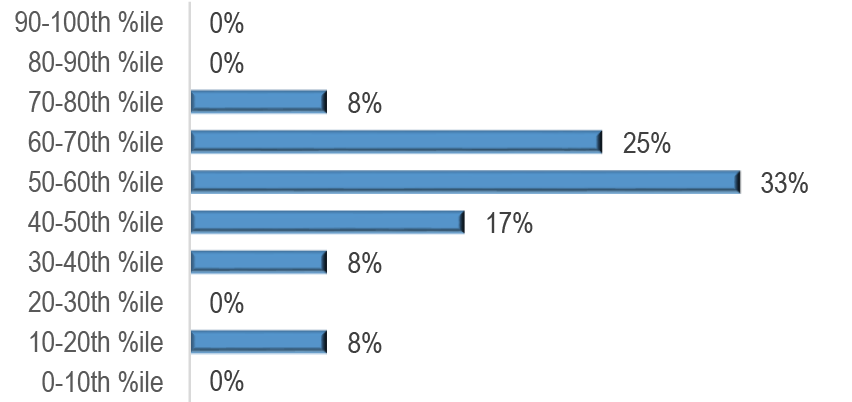

Figure 1: What is your current equity positioning or sentiment in historical terms, expressed from most bearish (0th percentile) to most bullish (100th percentile)?

Source: J.P.Morgan

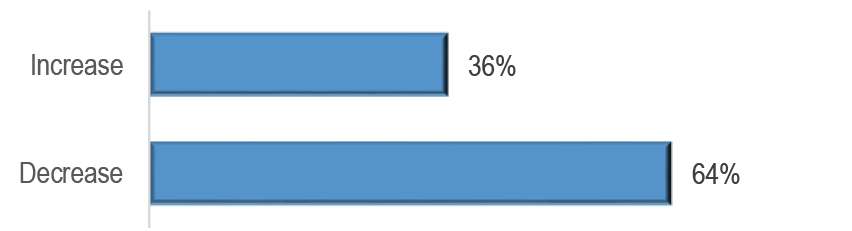

Figure 2: Are you more likely to increase or decrease equity exposure over the coming days/weeks?

Source: J.P. Morgan.

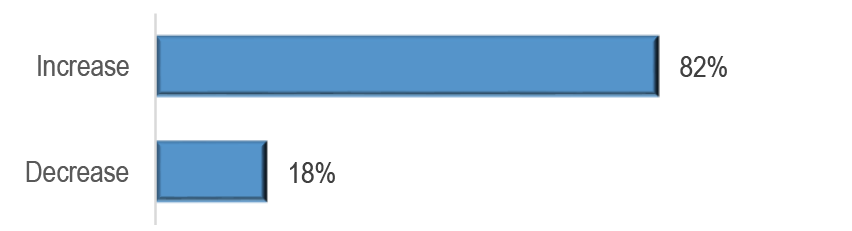

Figure 3: Are you more likely to increase or decrease bond portfolio duration over the coming days/weeks?

Source: J.P. Morgan.

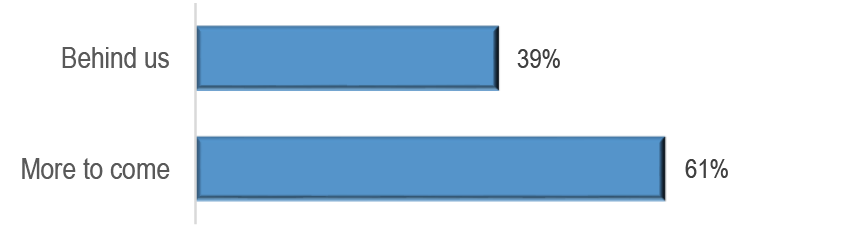

Figure 4: Do you think the market reaction to recent elections in EM (Mexico, India, South Africa) is behind us, or is there more to come?

Source: J.P. Morgan.

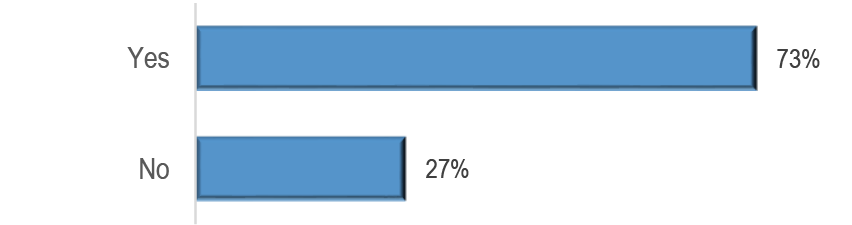

Figure 5: Do you believe markets are underpricing the risks around remaining elections this year (e.g., US, UK, France)?

Source: J.P. Morgan.

Figure 6: Do you think the recent decline in oil was driven primarily due to a reassessment of fundamentals, or technical flows?

Source: J.P. Morgan.

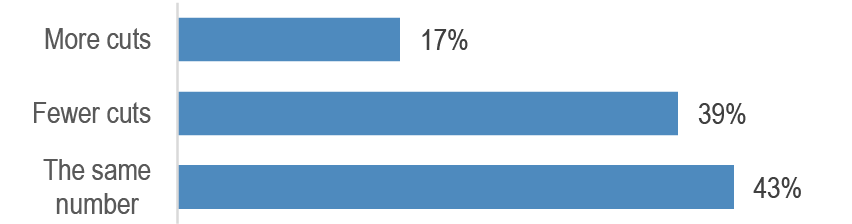

Figure 7: Do you expect more or fewer ECB cuts this year following the June ECB meeting, compared to your expectations prior to the meeting?

Source: J.P. Morgan.

JPM Clients’ View - This Week’s Interim Survey Results

The charts below show interim results from this week’s survey, collected over the first ~24 hours it was live. The survey remains open here, and we will show updated results in the next J.P. Morgan View publication

Figure 8: What is your current equity positioning or sentiment in historical terms, expressed from most bearish (0th percentile) to most bullish (100th percentile)?

Source: J.P.Morgan

Figure 9: Are you more likely to increase or decrease equity exposure over the coming days/weeks?

Source: J.P. Morgan.

Figure 10: Are you more likely to increase or decrease bond portfolio duration over the coming days/weeks?

Source: J.P. Morgan.

Figure 11: Do the French elections have systemic implications for the broader Eurozone?

Source: J.P. Morgan.

Figure 12: Would a large majority win in the UK elections be positive or negative for UK assets?

Source: J.P. Morgan.

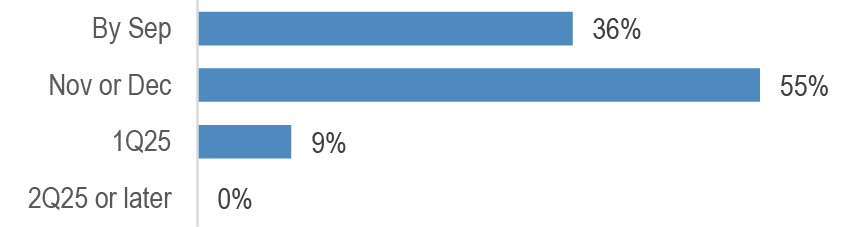

Figure 13: Following last week’s CPI data and FOMC, what’s your current expectation for when the Fed will first cut rates?

Source: J.P. Morgan.

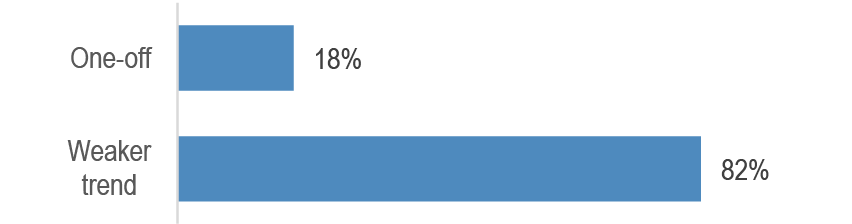

Figure 14: Do you believe the weakness in US May CPI and PPI was a one-off or the start of a weaker trend?

Source: J.P. Morgan.

Long carry/short volatility trades are being unwound

While global equity markets continued to drift higher over the past week, there have been divergences and the macro picture has become rather confusing due to conflicting indicators.

Both US CPI and PPI inflation posted significant negative surprises bolstering hopes of Fed rate cuts and thus a soft landing. It is difficult to tell at this point whether these negative inflation surprises were one-offs or the beginning of a new trend of benign US inflation prints. Given the May US CPI/PPI surprises were largely driven by a few components such as air fares and car insurance, our bias is to view these inflation surprises as one-offs.

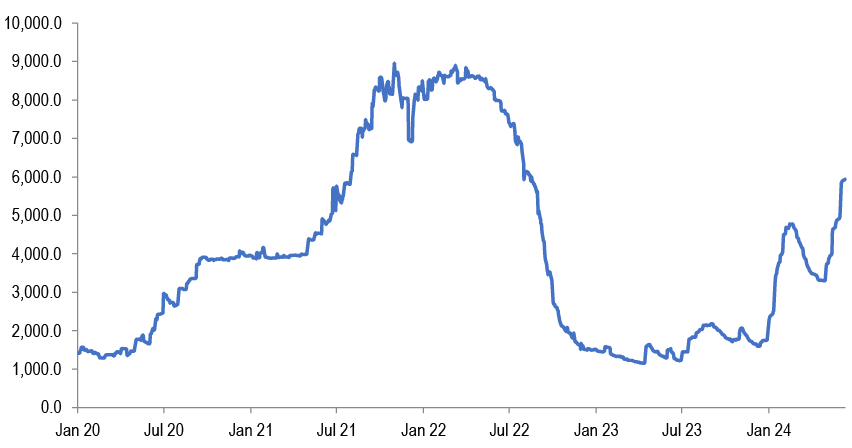

Outside these components, US services inflation remains elevated and in goods space the continued rise in global shipping costs is likely to put upward pressure over the coming months. Figure 15 shows that global shipping costs continue to rise, surpassing the previous highs from January.

On the growth front, while the picture outside the US remains solid, the latest US labor market indicators send conflicting messages. While the US payroll survey was strong, the US household survey and weekly initial jobless claims are conveying a more negative picture. While our bias is to put more weight on the US payroll survey, the recent rise in weekly jobless claims is concerning to us and their trajectory needs to be watched closely over the coming weeks. If the US weekly initial jobless claims fail to go back down below the 230k mark and instead they continue to drift upwards, then US recession fears will likely re-emerge unsettling risk markets.

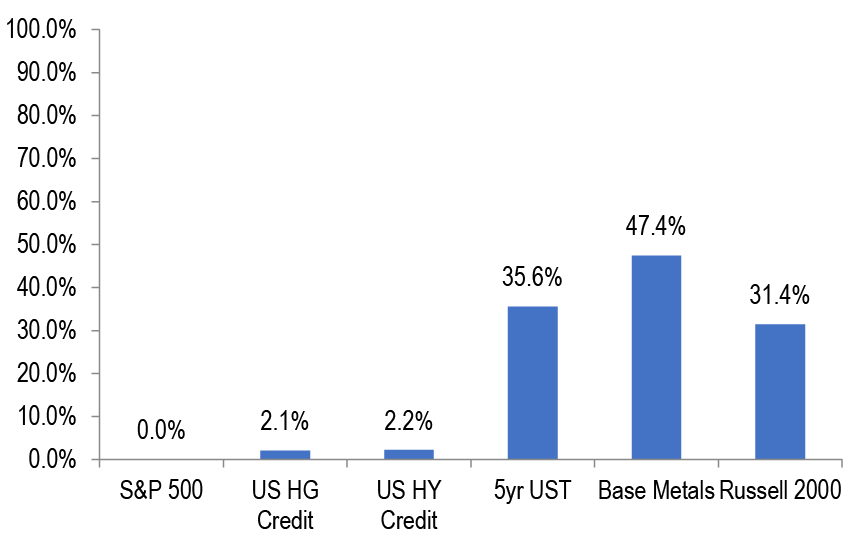

This shows how narrow the soft landing scenario is. While last week’s benign US inflation prints reinforce the soft landing scenario, if a significant softening of US labor markets is taking place at the same time, the combination could quickly see market participants becoming concerned about a near term US recession. And as we argued previously in our publication, very little US recession risk is currently priced in across risk assets. To gauge US recession risk our approach has been to compare the current cycle peak to trough declines of equity indices to those seen during previous recessions. Given the higher cyclicality and interest rate sensitivity of small caps due to their greater reliance on floating rate debt, that makes them a more suitable place to gauge cyclical risks. The average peak to trough decline for US small caps has been around 33%, over the previous twelve US recessions, only modestly worse than the 29% seen for the S&P 500. Since its January 2022 peak the Russell 2000 small cap index has declined by around 10%, mechanically implying 10%/33%=31% probability of US recession ( Figure 16). In other words, our simple framework implies that small caps price in rather modest probability of US recession. And most other asset classes including the S&P 500, price in even lower probability of US recession.

Another headwind for markets is the emergence of political risk. After Brazilian, Mexican, Indian, South African political/policy risks, French political risk has emerged as a headwind for not only French assets but also euro assets more broadly. While polls hint at a possible Le Pen victory in the coming French lower house election, the outcome of the French election remains uncertain with alliances currently being built in both the right and the left. A new program was released yesterday from Le Pen National Rally party and there were some significant shifts. On the fiscal side, the party wants to reduce electricity prices and lower the VAT rate on gas and fuel prices, while the party originally wanted a lower VAT rate for a much larger set of items. Separately, party leader Bardella argued that the retirement age would not be lowered. These shifts suggest that the risk of a very large fiscal slippage is likely less significant than first anticipated. On the negative side the program is short and lacks many details to make a proper assessment (see latest note by our colleague Raphael Brun-Aguerre, June 14th). More importantly, a dysfunctional cohabitation between the President and a Le Pen government could result to new lower house election within a year, prolonging political uncertainty.

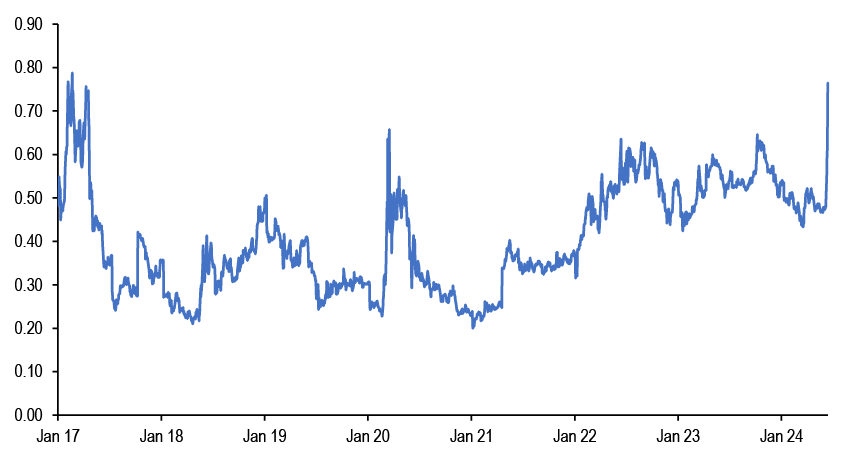

The market reaction has so far been focused on French assets. As shown in Figure 17 the largest position reductions have been in French government bond futures followed by CAC40 futures. There has been a more modest de-risking in other futures contracts, thus suggesting that so far investors see the coming French election more as a local problem rather than a systemic problem for the eurozone. That could change however if the rhetoric from Le Pen’s party starts becoming more anti-EU, for example in a scenario where a Le Pen led administration challenges the EU framework.

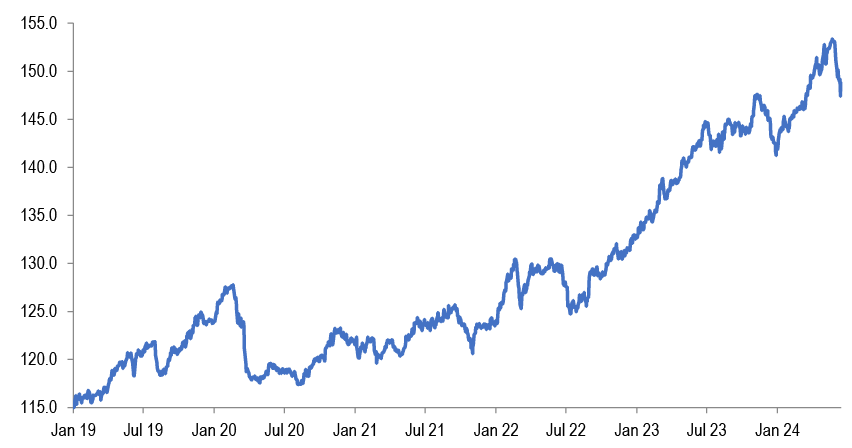

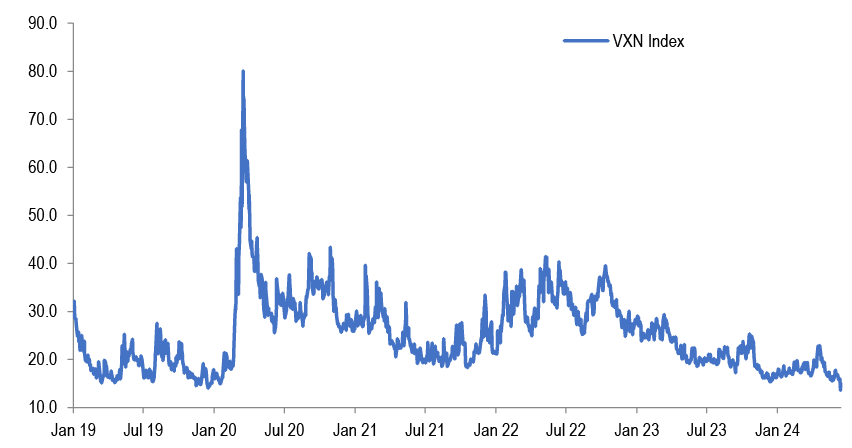

The widening of the French-German 10y government bond yield spread to the highest level since the French presidential election of 2017 ( Figure 18) looks set to continue for at least a few more weeks until the coming French election at the beginning of July. In our opinion this widening of the French-German government bond yield spread is not an isolated phenomenon, but part of a broader trend of unwinding of certain long carry /short vol trades due to political risks. This includes the widening of peripheral euro area sovereign spreads as well as the weakness in crowded EM carry trades such as previous long positions in Mexican peso. The recent weakness in Mexican peso is an example of the unwinding of a sizeable FX carry trade that was previously building up for two years, from mid 2022 to end-May 2024 ( Figure 19). Ultra low equity vol is another manifestation of the crowdedness of the carry trade in equity space in particular in the US ( Figure 20), which is at risk of being unwound if political/policy headwinds intensify into this year’s US presidential election. While we see little implication for UK assets from the coming UK general election, the balance of risks is skewed to the downside in a scenario where a Labour government raises more taxes than those outlined in its manifesto, in particular capital gains taxes.

An additional headwind for markets stems from liquidity as central banks shrink their balance sheets. While the BoJ delayed details of its QT process to July meeting, it appears to be looking to shrink its JGB holdings at a much faster pace than the current market expectation of a bit over JPY10 trillion per year. And this adds to the liquidity reduction from other major central banks. Even as the Fed is reducing its QT pace, the ECB looks set to offset some of that decline by shifting to partial reinvestment of its PEPP portfolio in 2H24 and ending reinvestments at the turn of the year. While we had previously noted that net sales by G4 central banks look set to continue at a monthly pace of around $100bn for the remainder of the year, the BoJ’s QT could lift this pace to $110bn-$120bn per month pace.

Liquidity looks also weak in EM. In China in particular, M2 money supply growth moderated further to 7.0%oya in May, translating to a modest sequential increase of 0.3% m/m sa vs. contraction in April, which was the first monthly sequential contraction in around ten years. M1 growth was weaker, turning negative in April and further decelerating to a new record low of -4.2%oya in May. The gap between M1 and M2 growth, a usual leading indicator for the business cycle, fell to -11.2%-pts. While technical factors such as the crackdown on interest rate arbitrage and the absence of households’ demand deposit from China’s M1 statistics might be partly responsible, the collapse in M1 growth could be an indicator of weak sentiment in the corporate sector (amid lack of investment opportunities, corporates will keep deposits more in time deposits than in demand deposits), thus posing downside risk to Chinese equities.

In all, we maintain a defensive stance. While the benign US CPI and PPI reports provide some relief, they were largely driven by a few components such as air fares and car insurance and our bias is to view these inflation surprises as one-offs. Political and liquidity risks pose downside to crowded long carry/short vol trades including the US equity trade, which is at risk of being unwound if political/policy headwinds intensify into this year’s US presidential election.

Figure 15: Shipping Index by Compass (XSI-C) - Far East to US West Coast

Source: Bloomberg Finance L.P., J.P. Morgan.

Figure 16: Probability of a recession as it was priced on June 13th 2024 across US equity, credit and rate markets

In %.

Source: Bloomberg Finance L.P., J.P. Morgan.

Figure 17: Implied position changes based on the proportional change in open interest over June 10th - 13th across various futures contracts.

% of open interest as of June 7th. See text for details about the constructions of this metric.

Source: Bloomberg Finance L.P., J.P. Morgan.

Figure 18: France-Germany 10y government bond yield spread

Source: Bloomberg Finance L.P., J.P. Morgan.

Figure 19: JP Morgan FX Carry 5% volatility target index

The latest tariffs announcement by the Biden administration confirms the increased use of industrial policy, and in our view, any prolonged export restriction on critical minerals will accelerate the rise of alternatives to China. There are three reasons for the US to remain optimistic. First, more opportunities exist to diversify critical mineral suppliers than it is for oil. Second, strengthening strategic stockpiling by the US government and corporates can act as a buffer against sudden supply chain disruptions in the near term. Third, technological innovation and recycling has the potential to relieve pressure on primary supply over the long term.

Investors remain sanguine on the outlook for the global economy and markets. More than 70% of investors expected a soft landing. Stretched valuations and risks of a market sell-off are seen as greater risks than longer-term debt sustainability or geopolitical risks from the China and the upcoming US elections. The European elections will have little impact over the near term. Europe needs to address structural weaknesses to boost competitiveness and there has been too much focus on cyclical factors. Trump 2.0 could be worse than Trump 1.0 for Germany as Chancellor Scholz has made a point of closely aligning himself with Biden, and it’s too early to call the outcome of the US presidential elections.

We believe a potential Labour victory in the upcoming elections is likely to be net positive for the market. Labour agenda is modestly pro-growth, but crucially with a likely cautious fiscal approach. Labour have also sought to reassure businesses by ruling out corporation tax increases. At sector level, we see a Labour win as a positive outcome for Banks, Homebuilders and Food Retail, while Energy and Transportation are likely to trade negatively as a result of Labour’s policies. Overall, UK equity market (OW) is trading cheap, it is a low beta play, has China exposure, and the highest dividend yield out of all large DM markets.

Across asset classes, we find evidence of large position reduction in French government bond futures followed by CAC40 futures. There has been a more modest de-risking in other futures contracts thus suggesting that so far investors see the coming French election more as a local problem rather than a systemic problem for the eurozone. Spec investors including momentum-based investors played a significant role in the recent retracement in Chinese equities, particularly in the offshore HSCEI contract.

Besides cutting out the May statement’s discussion of changes in the balance sheet reduction plan, there was only one other change in the post-meeting statement. While the May statement referred to “a lack of progress” toward two percent inflation in recent months, FOMC’s post-meeting statement describes “modest progress.” The median dot did not surprise hawkishly for the out years, projecting another four cuts next year (up from three in March) and four in ’26 (also up from three in March). We continue to look for a first ease in November, and perhaps see risks tilted a little more toward September than December.

The extent to which a possible Le Pen led administration would challenge the EU framework, as opposed to working within it, is hence still a key call and also still unclear. The EU and more specifically Euro area institutions have travelled a long way since the regional debt crises. There is now a deeper set of tools to address funding challenges and more shared understanding between North and South of the right balance between constraints on policy versus supports for countries in distress. At the same time, political parties on the right who had previously been fiercely critical of the EU and its institutions have toned that criticism down.

With the BoJ’s signal for a “substantial” reduction in its JGB purchases, we believe that the BoJ raised the bar for a July rate hike. Governor Ueda didn’t rule out the possibility of a rate hike in July, stating that the BoJ would decide based on the economic and inflation developments up to that point. As the BoJ is pursuing gradual policy adjustments, it likely will prefer to avoid causing large shocks to the market by making a simultaneous decision of a rate hike and a “substantial” QT. We now see the rising risks for the BoJ to delay rate hikes until September unless an additional weakness of the yen puts more pressure on the BoJ.

Spreads are a bit wider here and a bit tighter there but, overall, the nuances and narratives remain little changed across the global credit complex. Optically, spreads are thin, though maybe not quite as thin as they first appear adjusted for quality and ongoing benign default risk. What keeps the show on the road, of course, is that all-in yields remain in place, which continues to garner the support of the institutional investor base, making lower yields a bigger market risk than higher yields.

President Macron’s decision to call for lower house elections has surprised markets, as is evident in the reaction from rates. The key issue for markets is idiosyncratic fiscal slippage in a Le Pen majority rather than an existential one such as Frexit. The FX market reaction should thus be lower intensity than in 2016-17. It also helps that, unlike then, rate differentials are not moving substantially against the euro. Local markets rather than FX should be more vulnerable, but the euro will still be sensitive to any further escalation. The rule of thumb is that EUR/USD weakens by ~0.5% weakening for every 10bp of widening in the periphery.

We continue to embrace a range-trading mentality and do not feel compelled to chase the move to lower yields for now. Given the implications for PCE, we think it’s less likely yields can revisit their late-May highs, and the bar for adding duration is likely lower than it was even a day ago. However, with yields at the bottom end of well-established ranges and valuations no longer cheap in our fair value framework, we prefer to be patient before turning tactically long. If the front-end of the inflation curve continues to cheapen, we would look for opportunities to add long exposure, particularly in a carry-efficient form.

India local markets will provide investors with a very compelling opportunity, having the second largest local debt stock amongst all index members, the highest index duration, and an above average nominal yield (against one of the lowest levels of bond volatility across all of EM). In this extensive local market guide, we provide investors with a detailed analysis of the inner workings of the local FX and bond markets, take a deep dive into the intricacies of monetary policy and central bank liquidity management, as well as lay out a framework for thinking about how the domestic economy will evolve on a forward-looking basis.

In our 12th annual Retail vs. AMZN deep dive, team Retail and Internet both expect e-commerce penetration to rise with ~8% sales growth in 2024 (favoring WMT and AMZN) and medium-term e-commerce expanding ~2x that of core retail sales. Two factors that favor e-commerce growth this year: a gen merch sales rebound as share of wallet headwinds fade and consumption trends approach wage growth plus a consumer that is value seeking vs. “browse shopping.”

Our sector teams assess their coverage exposure to France, FX sensitivity to the EUR and detail the potential single stock implications. The results of the EU Parliamentary Elections saw a significant increase in the number of seats of the far right. This was particularly the case for France. Our Economics team also highlighted the risk that a majority emerges outside of Macron’s party, which would mean Macron would need to nominate a prime minister corresponding to the new majority.

Using the new exclusion criteria, we find 90 stocks in MSCI Asia ex-Japan will no longer be eligible for ownership by European ‘ESG’ investors. Looking forward, it is likely a portion of funds opt to remove the ‘ESG’ moniker rather than comply with the strictest exclusions. Instead, we expect a degree of re-labelling with greater emphasis on terms such as ‘transition’ which is subject to less onerous exclusion criteria and more aligned with the approach we see European ESG investors already take in Asia.