The J.P. Morgan View : Market prematurely settling back into soft landing narrative

This document is being provided for the exclusive use of blake@sandboxfp.com.

15 May 2024

The J.P. Morgan View

Market prematurely settling back into soft landing narrative

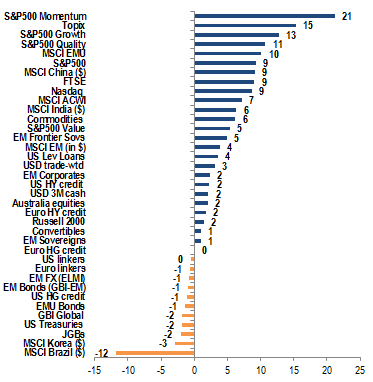

YTD returns by asset

Source: J.P. Morgan.

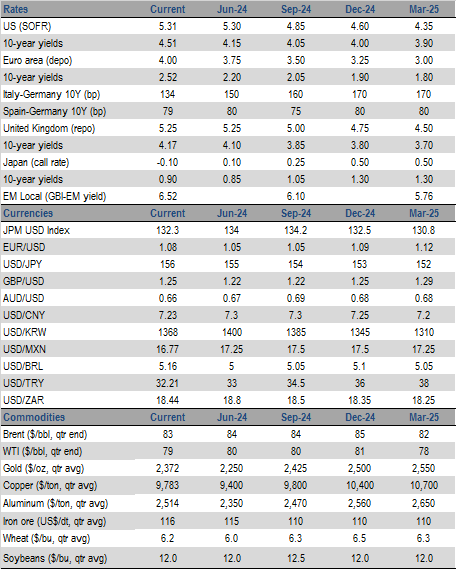

Cross-Asset Strategy: The 2024 global election cycle is just warming up, with elections still remaining across key geographies including the US, UK, India, Mexico and South Africa. In the US, a loss for the incumbent could drive substantial changes in trade policy, foreign policy, regulation, and fiscal/tax policy. In equities we constructed thematic equity baskets to hedge various policy outcomes, and in commodities we note a change in the administration could mean a lighter regulatory burden on oil and gas companies, and bearish risk for base metals prices and agri commodity exports due to the potential for a re-escalating tariff war and stronger USD. Last week was relatively light on major data releases, with stronger than expected longer-term inflation expectations in the US, and the ECB April meeting minutes reinforcing the sense that the ECB is set for a June cut. We stay neutral duration outright in the US and Eurozone ahead of inflation data this week but keep on steepeners. In the UK, the BoE provided a dovish tilt despite stronger data; we keep SONIA curve flatteners as a positive carry bullish proxy. While cautious EM policy rate cuts continue, the scope for cuts in 2H24 has diminished, particularly in Asia, so we stay neutral local duration. US HG bond spreads rallied despite a surge in issuance given strong demand, indicating robust technicals. In Euro credit, we expect to continue to trade rangebound over the near term as we are currently in a ‘bad news is good news’ trading environment. In FX, the medium-term view is still bullish USD on high yields, growth cushion and other supports, but tactical concerns stem from nascent signs of fading US growth exceptionalism and saturated investor longs.

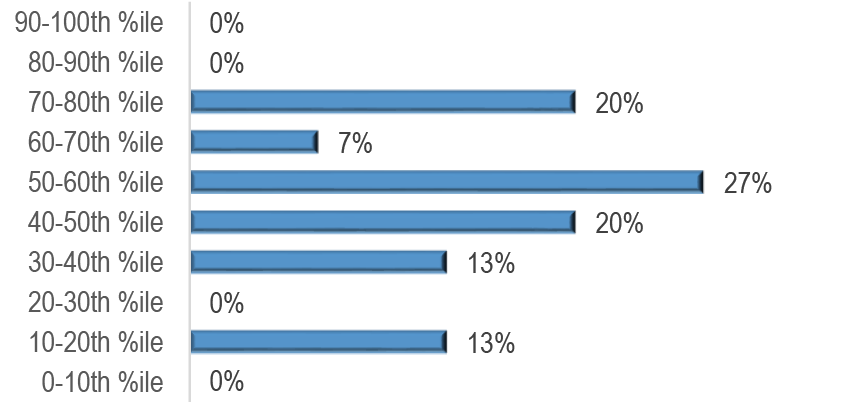

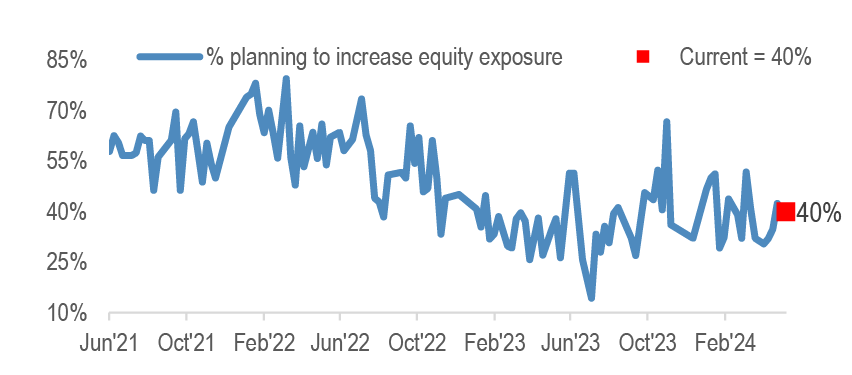

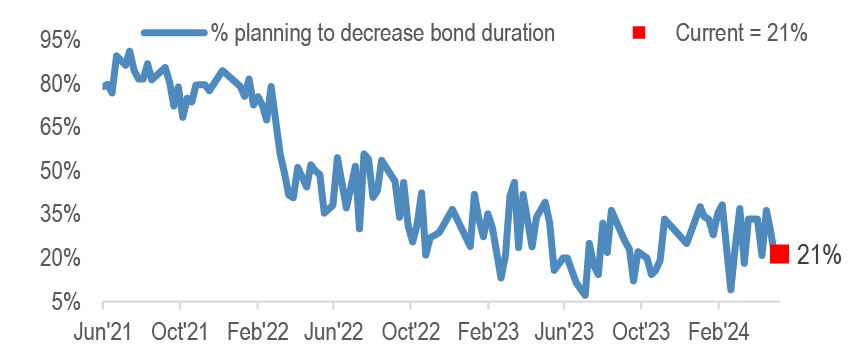

JPM Clients’ View: Click here to take this week’s survey. This week we poll investors on China equities, jobless claims, DM CBs and USTs, in addition to our running sentiment questions. Our last survey results indicated: (1) equity exposure/sentiment among respondents is ~50th percentile on average; (2) 40% planned to increase equity exposure, and 79% to increase bond duration near term; (3) 57% believe the 160 level on JPY is a line in the sand for the Japanese MoF; (4) the median expects Fed QT to end in 1Q25; (5) most respondents (53%) have high confidence the ECB will cut in June.

The market is settling back into the soft landing narrative after softer US jobs data and dovish guidance from the Fed, ECB and BoE. However, the macro outlook is uncertain and for equities we are entering into a seasonally tricky time of the year, with a challenging combination of inflation at risk of staying too high, profit margin pressures, and elevated positioning.

New Trades: Initiate TIPS breakeven wideners (White), long HYG volatility (Wu).

Upcoming Catalysts: Fed speak (all-wk); Japan PPI (5/13); US PPI, German ZEW (5/14); US CPI & retail sales, Eurozone GDP (5/15); US jobless, housing starts & IP (5/16); US leading index, China IP & retail sales, Eurozone CPI (5/17).

Cross-Asset Strategy

Economics

Expecting moderation in growth and inflation this quarter to levels consistent with resilience and persistence. We are anticipating a modest rebound in US GDP growth to a 2.5%ar this quarter even as soft April business surveys and signs of moderating labor demand have increased downside risks. Outside the US the growth remains imbalanced as the recent consumer spending lift has been driven entirely by the EM. With spending stalled in W.Europe and Japan and consumer confidence readings still depressed across the DM, sustaining this pickup is by no means assured. On inflation, a 1Q24 acceleration in core CPI gains to a 3.5%ar aligns with our view that the global disinflation process is now stalling. Sustained strong service-sector demand and elevated labor costs looks likely to limit any fall in service price inflation. We also see core goods inflation moving modestly higher. In all, we project global core CPI to rise 3.2%ar in 2Q24. The limited April releases so far are broadly consistent with this view.

A shallow Western European easing has begun. Following the SNB cut, the Riksbank lowered its policy rate last week. The ECB April meeting minutes confirmed that a June cut is on track while the BoE’s dovish hold last week opened the door to a possible June ease. While European easing is getting underway, the latest signs show a pickup in growth and sticky inflation for the ECB and BoE. For the Riksbank the case for a substantial easing is stronger, but external pressure on the currency may also slow its path (GDW, May 10th).

Equities

Better China trading could have some more to go. While we do not believe that the longer-term structural concerns are finished, the more positive China trading could last through summer on increasing market hopes that the worst of housing weakness may be behind us, and until the US elections heat up. EM investors remain UW China and valuations have another 10-15% upside before closing the discount to historical. Mining and Energy remain interesting as a way to position for more positive China trading. Metal prices are likely to be supported by low inventories and better demand, and commodity equities offer a high FCF yield and attractive valuations (Equity Strategy, May 12th). Chinese equities’ rally continued last week on more favorable policy actions, that are in the general direction of raising demand, curbing supply and raising prices over certain utility-type services, plus solid trade data (China Equity Data Tracker, May 10th).

Equity implications of upcoming global elections. The global election cycle is just warming up, with 60 of 77 elections still remaining across key geographies including the US, UK, India, Mexico and South Africa. Macro themes remain dominant, while focus is beginning to center on the US Presidential and Congressional elections given the policy differences between the leading candidates, the size of the US equity market, and the potential knock-on effects to other geographies, particularly in EM. In the US, a loss for the incumbent could drive substantial changes in areas such as trade policy (e.g. US-China), foreign policy (e.g., Middle East/Israel, Russia/Ukraine, etc.), regulation (e.g. environment/energy, anti-trust) and fiscal/tax policy (e.g. TCJA sunset on 12/31/25). We constructed thematic equity baskets to hedge or position for various policy outcomes (Global Thematic Strategy, May 7th).

Entering into seasonally tricky time of the year, on top of a challenging combination of inflation at risk of staying too high and profit margin pressures. The Goldilocks view that market embraced in Q1 of inflation/rates moving lower but at the same time of earnings acceleration and economy having no landing remains an inconsistent one. We look for more of a consolidation in equity markets over the next months. We believe that the gap that has opened up YTD between Fed and the equity market needs to close (Equity Strategy, May 7th).

Japanese equities’ downward pressure due to the yen’s rapid depreciation has eased for now. Earnings results featured many companies announcing increased shareholder returns and RoE targets. One-year on from TSE-led reform demands have led to rise in weighting of companies with PBRs above 1.0x from 50% to 60% and improvement in RoE of low-RoE names (Japan Equity Strategy, May 7th).

In SMids, we adhere to our cautious view since: 1) historically interest rates have not moved lower in short order; 2) growth may not save the day because it appears weaker this time around; 3) we don’t see enough of a return to warrant taking on equity risk at this juncture. SMid-Caps (and Large-Caps for that matter), in most regions of the world seem unlikely to beat the return of 20-yr US Treasuries from here to the next recession. Japan is the only SMid mkt that seems to offer a rerating story at present (SMid Alpha, May 7th).

US election’s qualitative debate with EM investors is bear-biased on the re-edition of “America First”, the risk of higher tariffs, and the collateral damage of those policies on the inflation outlook. The US election could become an obstacle that conflicts with the view that the US will slow and cut rates into year-end, favoring EM equities (EM Lighthouse, May 8th). 1Q24 EM results overall have been positive. For next quarter, we think the 4 broad macro variables are positively biased: increasing operating leverage, rising commodities, declining 10Y UST, and the consolidating USD bull run (EM Lighthouse,May 6th).

Bonds

Bonds saw a modest bear flattening over the past week. In the US, the week was light on major data releases, with stronger than expected longer-term inflation expectations in the Michigan survey rising close to its recent highs at 3.1%. While valuations look cheap, in the near-term yields are likely somewhat sticky as it will take moderating inflation data to validate dovish Fed expectations. We stay neutral duration ahead of inflation data and look to add bullish front-end exposure on further yield rises, and keep 5s/30s steepeners to position for eventual easing and higher term premia.

In the Euro area, the minutes of the April meeting reinforced the sense that the ECB is set for a June cut. Over the medium term, we retain a bullish stance given an approaching start to a cutting cycle and gradual easing thereafter, but the lack of near-term catalysts keep us neutral for now. We keep steepeners via 10s/15s Germany and 2Yx2Y/10Yx10Y EUR swaps. In the UK, the BoE provided a modestly dovish tilt despite stronger data; we keep fronts/reds SONIA curve flatteners as a positive carry bullish proxy.

In EM, near-term growth prospects remain solid, but the disinflation process has slowed and become more varied across regions. While cautious EM policy rate cuts continue, the scope for cuts in 2H24 have diminished, particularly in Asia. We stay neutral local duration and hold selective OWs in Brazil, Colombia, Uruguay, Czechia and Poland, offset by a short duration overlay and an UW in Thailand (EMOS, May 8th).

Credit

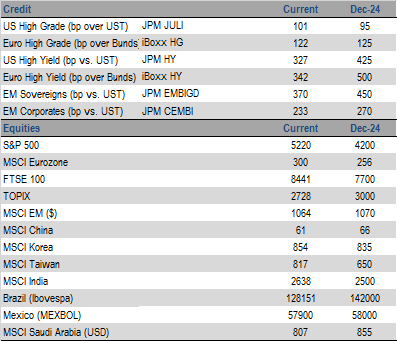

US HG bond spreads have been trading in a steady range of 100-107bps for the past 2M, recently closing at the tighter end of this range, while HG bond yields drifted lower. Spreads rallied last week despite a surge in issuance, with the largest weekly supply tally since mid-Feb’24. This indicates the robust technicals in the US HG bond market, with demand remaining strong even in the face of increased supply (CMOS, May 10th). The FOMC meeting outcome is a clear negative for most foreign buyers, as long-end USD yields fell significantly while hedging costs rose slightly with the prospect of less or delayed convergence between the Fed and other central banks. As a result, the JPM Foreign Attractiveness of USD IG Bonds index fell sharply to ~3M lows.

Our new monthly Spread Strategy Spotlight publication looks at credit and broader spread markets from the top-down. The first edition comes against the backdrop of the April US payroll and employment reports. Judged from the perspective of not-being-too-hot-nor-being-too-cold, the data could not have been better for spread and broader risk markets. We are not complacent but do not feel overly bearish with all-in yields remaining a powerful offset to optically thin spreads (Spread Strategy Spotlight, May 6th).

We expect euro IG to continue to trade range bound over the near-term. In our view, we are currently in a ‘bad news is good news’ trading environment, with the recent modest softening in the US data reducing the risk of a renewed policy hiking cycle (European Credit Weekly, May 10th).

Currencies

High-for-long would trump fading US exceptionalism. The medium-term view is still bullish USD on high yields, growth cushion and other supports, but tactical concerns stem from nascent signs of fading US growth exceptionalism and saturated investor longs. Inflation divergences will be key as central banks are inflation- rather than growth-focused. The upcoming US CPI will set the tone for FX as Fed pricing has been the single biggest driver of the dollar. Implications from a soft/firm US inflation print are obvious for the direction of Fed pricing, but more nuanced for USD. DXY has been more sensitive to inflation misses.

FX forecasts mostly unchanged: G10 unchanged ex-Scandis: EUR/SEK 1Q25 10.9 (10.3). EM: USD/ZAR 2Q 18.8 (19.0) upgraded on reduced election tail risks, EUR/CZK 3Q 25.75 (26.0) upgraded on hawkish CNB (KCV, May 10th).

Commodities

US Election Implications for Commodities. There could be little difference in overall macro direction between the candidates as extreme proposals are unlikely to materialize given the high probability of a split Congress. However, a change in the administration would mean 1) A possible major realignment of federal energy policy, which would likely not result in higher US oil and gas output but would lighten the regulatory burden on oil and gas companies. 2) US foreign policy could also see significant changes. 3) The potential for a re-escalating tariff war, particularly between China and the US, which is a major bearish risk for base metals via resulting FX and growth consequences. 4) For agri markets the prospect of a firmer dollar and potential trade tensions comes at an inconvenient time when the US is well stocked with a large export surplus of grain and oilseeds (Global Commodities, May 7th).

Turkey is playing a growing role in the European Natural Gas market. We expect Turkish domestic production to increase, theoretically freeing up LNG supply for delivery to Europe and Asia after the Ukraine/Russia transit deal ends. With ample import capacity and potential enhancements in export capacities, Turkey could export/transit up to 40 Bcm/year of natural gas to Europe by 2030 – a 60% increase from 2023 levels (European Natural Gas, May 8th).

This week, we poll investors on China equities, jobless claims, DM CBs and USTs, in addition to our running survey questions on equity positioning/sentiment, and intentions for near-term changes to equity allocation and bond duration. The results from the last survey are shown below.1

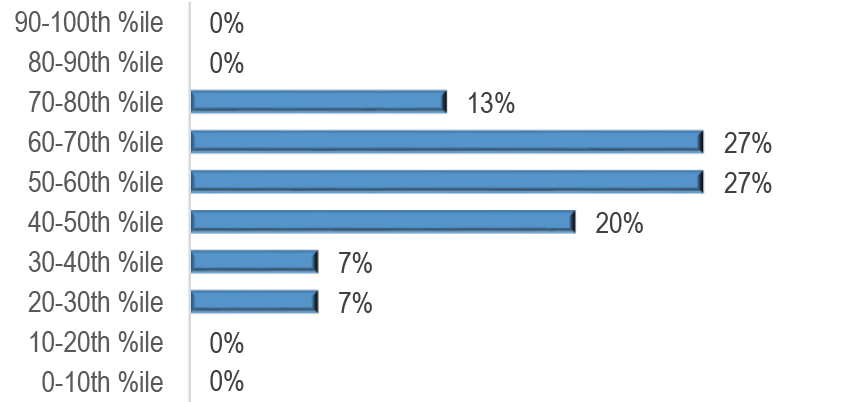

Figure 1: What is your current equity positioning or sentiment in historical terms, expressed from most bearish (0th percentile) to most bullish (100th percentile)?

Source: J.P.Morgan

Figure 2: Are you more likely to increase or decrease equity exposure over the coming days/weeks?

Source: J.P. Morgan.

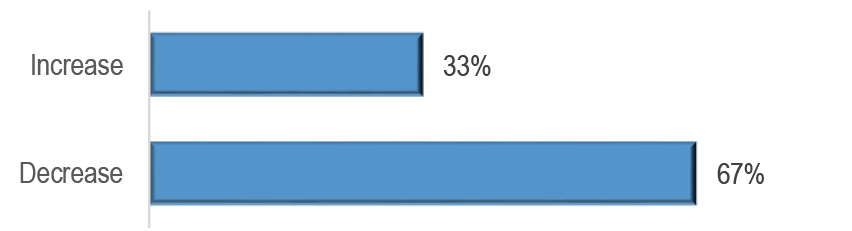

Figure 3: Are you more likely to increase or decrease bond portfolio duration over the coming days/weeks?

Source: J.P. Morgan.

Figure 4: Is the 160 level on JPY a “line in the sand” for the Japanese Ministry of Finance?

Source: J.P. Morgan.

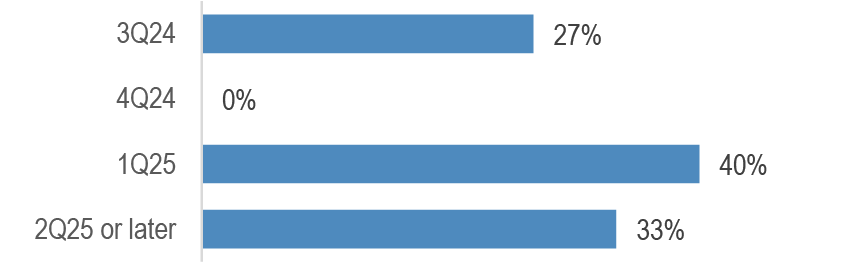

Figure 5: When will Fed QT end?

Source: J.P. Morgan.

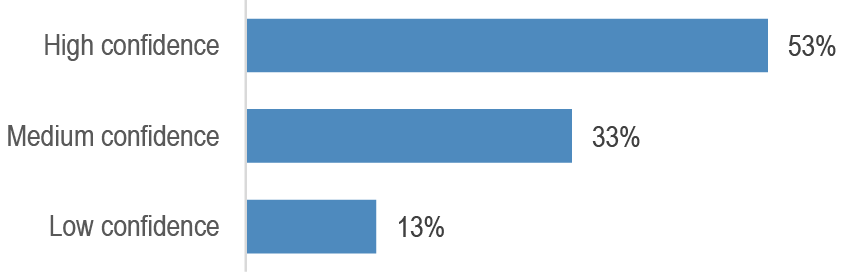

Figure 6: How confident are you that the ECB will cut rates in June?

Source: J.P. Morgan.

JPM Clients’ View - This Week’s Interim Survey Results

The charts below show interim results from this week’s survey, collected over the first ~24 hours it was live. The survey remains open here, and we will show updated results in the next J.P. Morgan View publication

Figure 7: What is your current equity positioning or sentiment in historical terms, expressed from most bearish (0th percentile) to most bullish (100th percentile)?

Source: J.P.Morgan

Figure 8: Are you more likely to increase or decrease equity exposure over the coming days/weeks?

Source: J.P. Morgan.

Figure 9: Are you more likely to increase or decrease bond portfolio duration over the coming days/weeks?

Source: J.P. Morgan.

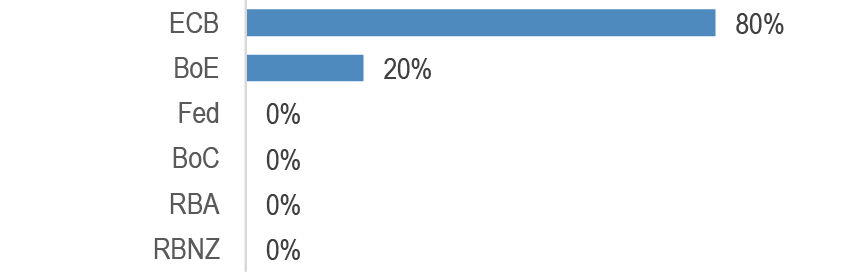

Figure 10: Is the rally in Chinese equities over the past 3M likely to continue?

Source: J.P. Morgan.

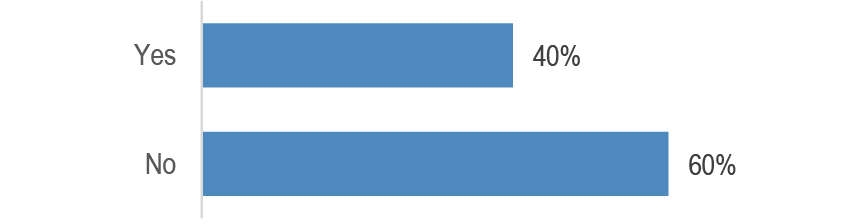

Figure 11: Do you find the recent softness in US jobs data (miss on NFP, jump in jobless claims last week) to be concerning?

Source: J.P. Morgan.

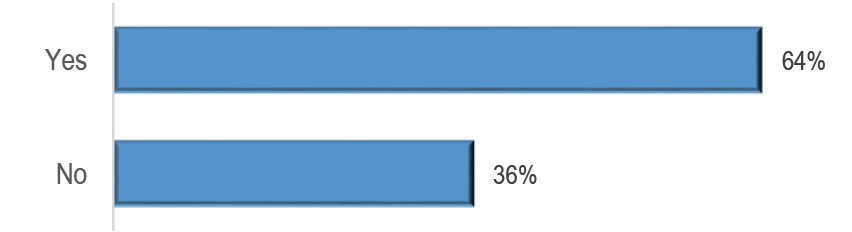

Figure 12: After the Riskbank and SNB, which DM central bank do you think will be the next to cut rates?

Source: J.P. Morgan.

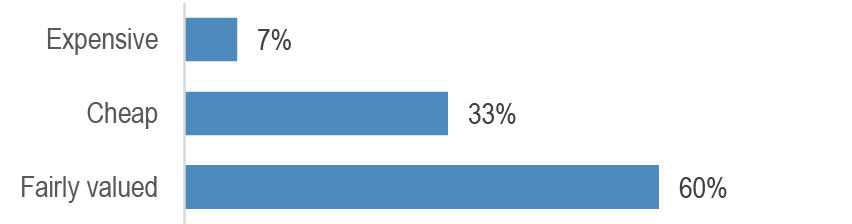

Figure 13: Are US Treasuries expensive or cheap at the moment, in your view?

Source: J.P. Morgan.

Market settling back into soft landing narrative

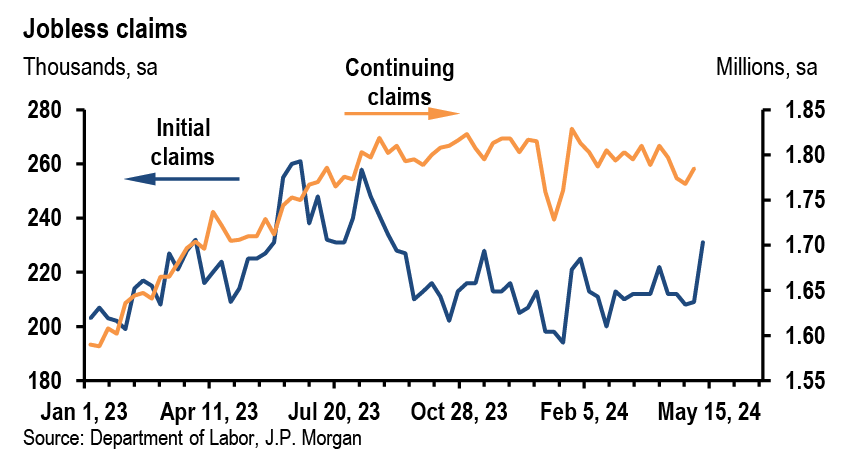

Initial claims jumped from 209,000 to 231,000 during the week ending May 4, a disappointing print that showed the highest weekly level for claims filings since last August. We are keenly focused on signs of labor market weakness but in this case, it is likely attributable to school spring break effects. The April jobs print at 175k has reassured the market that we are no longer in high for long, putting us squarely in soft landing. Meanwhile deterioration from NFIB Hiring Plans, JOLTS Private Hires and Construction series, would be worrisome if one extrapolates the downtrend, but this was countered by muted results from the JOLTS layoffs numbers.

Bonds seem have settled back in to the soft landing narrative after the scare from the March CPI print has finally been assuaged by less hawkish guidance from the Fed (effectively taking hikes off the table) and softer-than-expected US labor market, not to mentioned the dovish hold from the BoE. While we expected a synchronized cutting cycle earlier in the year, the high for long theme on the back of hot inflation prints produced a decoupling that pushed market’s expectation for the Fed’s first cut out to December and BoE out to September. This is now being dialed back as OIS market pricing points to first cuts in November for the Fed and August in BoE. Meanwhile, ECB probability of first cut in June has only increased from 85% to 91%. Despite our baseline view, we acknowledge the macro outlook is uncertain and the data, such as next week’s CPI and HICP, can evolve toward alternative scenarios. DM central banks contemplate a baseline scenario of soft landing where inflation converges to target allowing a gradual removal of restrictive policy stance, which would make carry trades attractive, such as long spread products and short vol, with a broad bullish stance. Alternatively, a hard landing scenario would produce a faster convergence to the neutral policy rate, arguing for outright long duration and steepeners, on the assumption of a bull steepening move. Finally, high for long can also come back into the picture if inflation proves to be stickier, and the suggested positioning would need to be short duration, with bear flattening and underperformance from the intermediate sector. Additionally, for equities we are entering into a seasonally tricky time of the year, with a challenging combination of inflation at risk of staying too high, profit margin pressures, and elevated positioning.

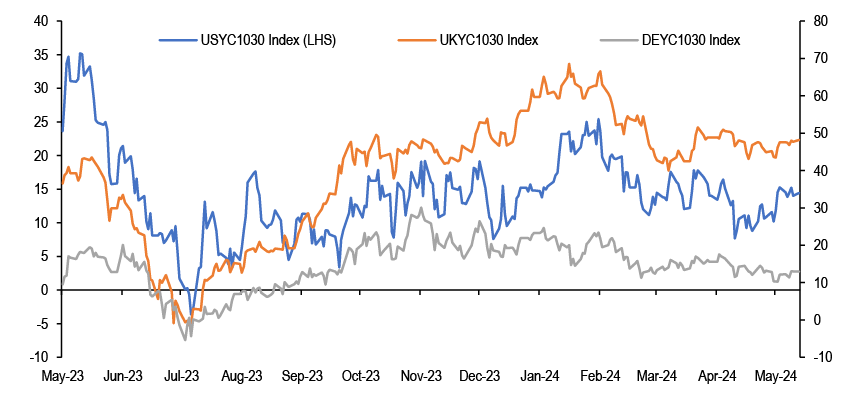

BoE left rates unchanged in a closer 7-2 vote as expected, but dovish language was added to the statement (“risks from inflation persistence are receding”) that more clearly opens the door to a June cut. We continue to assume an August start to cutting, as a lot of data are still to come, but the odds vs. June look more evenly balanced and the onus is now more on the data to talk them out of easing. In terms of positioning, we hold fronts/reds SONIA curve flatteners as a positive carry bullish proxy on 1Yx1Y SONIA, but conviction is lower given the 30bp rally in 1Yx1Y SONIA over the past two weeks and current valuations. We think both UK data (labor market 14 May, UK inflation data 22 May) and US data (i.e. April US CPI) will need to surprise to the downside to drive a further rally over the coming weeks. We continue to hold 10s/30s gilt curve steepeners with the curve a few bp too flat on a short-term regression basis vs. 1Yx1Y SONIA. There is no more 30Y conventional gilt supply scheduled for the rest of this quarter following the 2053 green gilt auction this week with 20Y and 40Y gilt supply remaining between now and the end of June, but given the recent rally in yields we are less sure of the strength of any outright duration demand in the 30Y sector. As discussed in our podcast, steepener trades should work a few months before and after rate cutting begins. Steepener trades in the UK, US, and Europe did well in the 2nd half of 2023, but gave back some p&l in 2024, shaking investors’ confidence. We believe these trades should once again do well on the assumption that the disinflation reasserts itself, clearing the path for rate cuts.

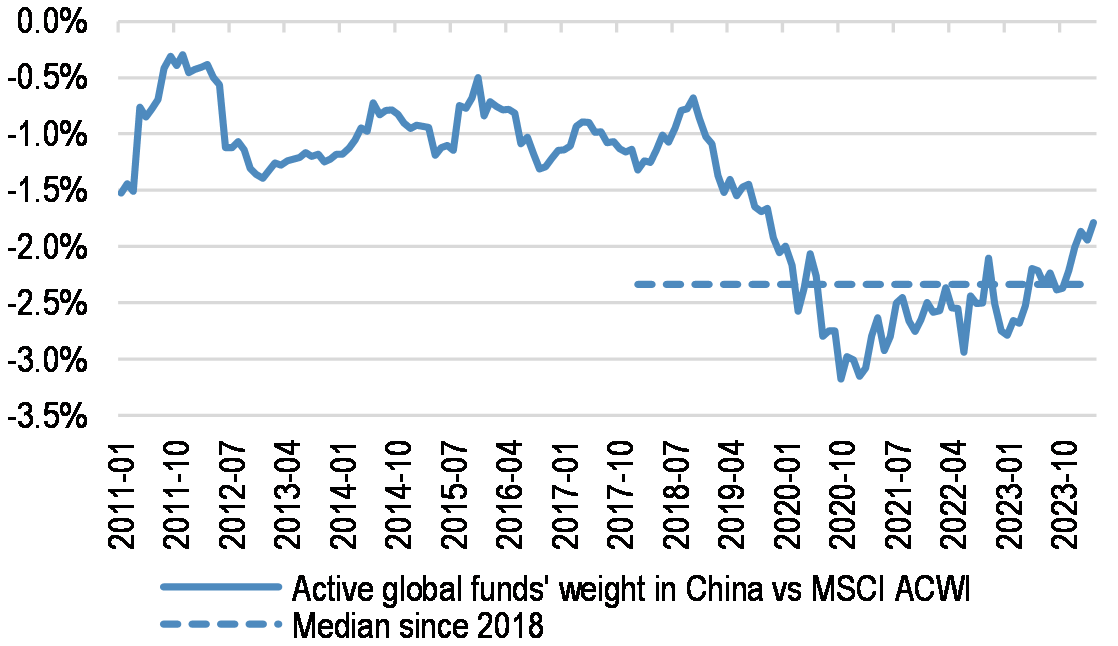

We continue to be tactically bullish on China, despite many caveats. In terms of the reason to be long, our Equities team continues to flag the cheapness, as China trades at 10.2x (-0.6SD below 10-yr average) and HK at 12.6x (-1.5SD below 10-yr average), so still cheap even after the recent rally since late-January 2024. In addition, the recent rally has still left China under-owned by institutional investors, and sentiment from clients has been broadly bearish. The UW positioning of managers is most obvious for global equity funds tracking ACWI and Asia Ex-Japan, not so for EM broadly, and the recent rally has prompted a partial catchup towards pre-GFC levels. It’s worth mentioning that improvements from China were a key input in reducing our UW to Eurozone Equities.

As to why the China equities view needs to be more tactical, we question the durability of the stimulus, as we expect the uplift to fade after the first quarter’s 7.4% q/q saar (moderating to 4% in 2Q24), and growth for the FY2024 settling to 5.2%. The overhang of housing is only partially mitigated by the easing of home purchase restrictions, where we would have preferred to see nationwide housing stimulus or some other form of help for consumers. Also, the technical analysis lens offers mixed messages, with RSIs in MXCN at ~80 a few days ago, indicating overbought conditions, but other measures of a stretched rally such as ‘current price as percent of the 200d moving average’ suggest there is further room to run. Meanwhile, the moves since mid-April have brought us to a place where we are well above moving averages, so no imminent worries of technical selling from going through key levels. One final consideration is the US election, which again argues for a tactical trade, as Chinese stocks can come under pressure once tariffs are back in focus.

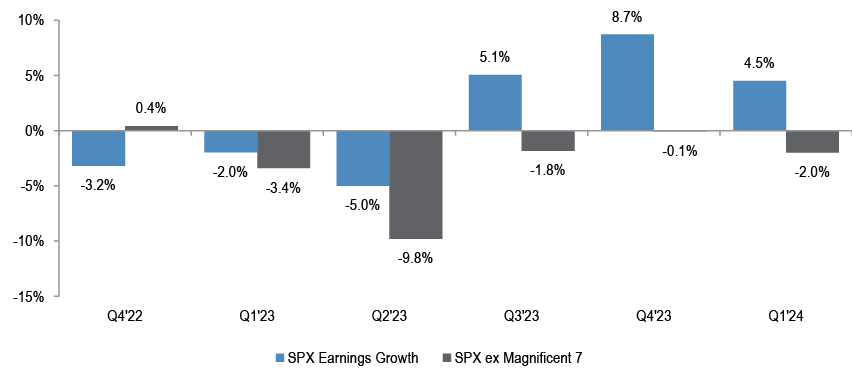

The earnings season is just about done, with 80-90% of companies having reported in US & Europe. Earnings growth came in better than consensus expected, at +5% y/y in the US, and -8% y/y in Europe. As we highlighted in previous weeks, the reward for beats has been subdued, while misses have continued to be severely punished. At a sector level, Discretionary, Communication Services and Tech continue to be the biggest drivers of overall earnings growth in the US. In fact, excluding Mag-7, S&P 500 EPS growth is -2% y/y, the 5th consecutive quarter of negative growth for the ex Mag-7 group. Meanwhile, the percent of companies guiding higher rose vs last quarter, and those guiding lower dropped dramatically. We don’t take comfort on the improved guidance, as the optimism on earnings has gotten ahead of the economic momentum.

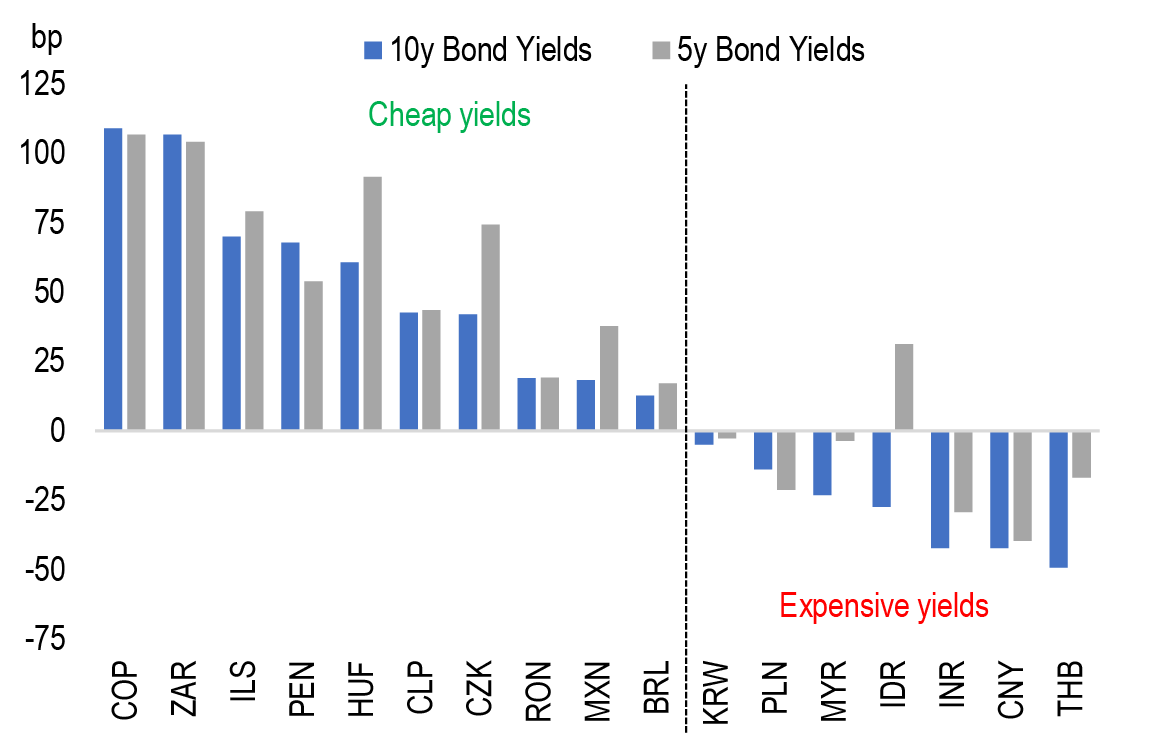

In Emerging Markets, we are in a holding pattern, being neutral on EM local rates, EM FX, EM Sovereign and Corporate Credit. EM growth is solid assuming a bounce in 2Q DM growth and reduced downside risk from China. Rate-sensitive markets have underperformed over the past month, and for both EM local and EM FX we did not manage to get oversold enough for a clear buy signal. As for the disinflation process, core inflation is already below targets in EM Asia, but has more to go in LatAm and EMEA, where core inflation will remain above targets through end-2024. The up-move in US rates has pressured EM currencies and challenged rate cut expectations, with EM Asia facing the most pressure, given rate differentials vs Fed at record lows. After the sell-off in EM Fixed income following the March 12th US inflation print, we see EMEA EM and LatAm local bond yields are above fair value, while Asia are generally below. So despite remaining MW on EM Local as a whole, we are OW EMEA EM and LatAm and UW in Asia.

Figure 14: Uptick in Jobless claims accounted for by school spring break

Figure 15: JOLTS Hires Rate, Private and Construction

Source: J.P. Morgan., Bloomberg Finance L.P.

Figure 16: Steepener trades did well 2H23, but 2024 has been a tough year to go long outright duration or steepeners

Source: J.P. Morgan., Bloomberg Finance L.P.

Figure 17: Active global equity funds’ position in China relative to MSCI ACWI

Source: EPFR, MSCI, J.P. Morgan estimates.

Figure 18: S&P500 vs S&P500 ex Magnificent 7 earnings growth

Source: J.P. Morgan Equity Research, Bloomberg Finance L.P.

Figure 19: Valuations of EM local currency bonds are attractive outside of Asia

With the global election cycle just warming up, we preview key upcoming elections and their implications across DM and EM. While macro themes remain dominant, focus is beginning to center on the US Presidential and Congressional elections given the policy differences between the leading candidates, the size of the US equity market, and the potential knock-on effects to other geographies, particularly in EM. In this report, we explore various election scenarios and provide 11 key thematic stock baskets, 11 stock screens and sector/style recommendations that align with major policy proposals across geographies. J.P. Morgan Research does not provide research coverage of baskets and investors should not expect continuous analysis or additional reports relating to them.

Conventional wisdom that geopolitical risks generate more noise than trend could be challenged by the ongoing shift to a multipolar world. The world is undergoing a large pivot in globalization compared to the prior 30-40 years with the pendulum shifting back to big and active government, protectionism, and income redistribution. Irrespective of the outcome of the US elections, US-China tensions are likely to escalate, but the tech competition between the US and China is at the epicenter of the rise in industrial policy along with the emerging doctrine on economic statecraft. “Mini fires” are often overlooked but have longer-term consequences to energy security, climate policy and immigration, particularly in the aid dependent zone around the Horn of Africa.

We conclude there is a lot of benefit to the ultimate buyers of financial services and products to keep things simple. One should not buy assets that are too complex to be easily understood as the risk is then that the asset will not be appropriate for one’s financial objectives. Second, the fewer the assets one has in one’s portfolio, the easier it is to judge risk on them, the easier it is to gauge one’s exposure, the easier it is to manage one’s portfolio and the less time it takes. And probably the greatest benefit of simpler products is that they are cheaper, in terms of management fees and the costs of buying and selling them.

Financial conditions steadily improved from their peak tightening in 2H22 to a net loosening by 4Q23. Moreover, this has been a broad-based improvement as the effect of past yield rises has faded, equity returns turned from a headwind to a tailwind and lending surveys have eased back significantly from their previous peaks. Based on quarter-to-date data for 2Q24 on 12-month changes to rates, spreads, returns as well as the 2Q24 lending surveys, this positive impulse from financial conditions appears to have continued. In all, the above suggests the financial conditions impulse remains positive, posing some upside risks for growth and inflation.

The ECB is likely to be agnostic and adjust its policy plans only if it sees evidence of significant market moves. At the same time, the domestic data are providing the main challenge at present: growth is improving without clear signs of improving productivity growth and services inflation is remaining sticky. We still see Euro area inflation eventually falling to 2% without the labor market having to weaken, but the path remains uncertain. To better balance risks, we take out an October cut from our forecast, taking this year's easing to 75bp and also modestly slow next year’s cuts, but without currently changing the endpoint of a 2% policy rate.

We stick with our call in August cut for now, but the odds vs. June look more evenly balanced and the onus is now more on the data to talk them out of easing. Given issues with the labour market and pay data at the moment, there is a greater focus on the services CPI in particular. This metric surprised the BoE by a significant +0.2%-pts in March. We also expect growth and activity to come in firmer than the MPC are projecting. A growth recovery appears to be underway, and this should be acting to reduce the urgency to cut rates.

The MoF continues to control the pace of yen depreciation through FX intervention, but it is becoming apparent that it can only slow yen declines temporarily. The weaker yen certainly brought benefits to the economy, but this has not yet led to a rise in overall domestic demand due to the clogging of the corporate-to-household income channel. Rapid weakening of the yen could potentially undermine confidence in the yen at home, which in itself may raise the risk of further weakening of the yen through a rise in capital outflows. We expect the BoJ to raise policy rates at a faster pace than hinted, to 50bp by end-2024.

In our view, it is in HK SAR’s interest to further deepen its financial linkages with the Mainland. Both cyclical and structural forces are at work. Current high interest rates are the major cyclical factor, which may last longer than previously expected. The structural challenges include China’s deflation pressure on corporate earnings, slowing potential growth in China, and geopolitical tensions. These may have prolonged effects.

Our broader Credit, Securitized Products and Public Finance Research teams collaborated and published their first edition of the new Spread Strategy Spotlight. These are either product- or regionally-focused, are published weekly and are focused on what our analysts judge to be the topical single-name stories of the day. By contrast, the Spread Strategy Spotlight will come at credit and broader spread markets from the top-down and be published monthly, initially at least. We are not complacent but do not feel overly bearish with all-in yields remaining a powerful offset to optically thin spreads.

We conclude that ultimately there could be little difference in overall macro direction between Trump and Biden and that most extreme proposals are unlikely to materialize given the high probability of a split Congress. A change in the adminstration would mean a possible major realignment of federal energy policy, which would likely not result in higher US oil and gas output but would lighten the regulatory burden on oil and gas companies. An escalating global tariff war could drag significantly on metals demand growth via slower GDP growth. Potential impacts of a change in US presidency in 2024 from a policy perspective appear the least severe for the agricultural sector.

Macro drivers such as policy rate differential and relative balance sheet dynamic are expected to be key drivers of the cross currency basis market, with limited beta to risk-off concerns and flight to quality dynamic. Widening on risk aversion and flight to quality expected to be temporary as occurring in a broad context of limited USD scarcity. Narrowing bias across cross currency basis from more than priced Fed easing and slower QT pace partly counterbalanced by risk of crowding out effect from increases in T-bill issuance, itself triggering some local USD scarcity, leaving broadly a neutral outlook.

We preview WMT, TGT, HD, and LOW’s 1Q earnings. WMT is trading at 25x our 2024 EPS forecast and 22x 2025E, suggesting its next move needs to be revision-driven, with at best one additional P/E turn on 2025E on a 4%+ comp. We are tweaking up TGT 1Q comp forecast to -3.6% (from -4.0%), and tweaking down HD 1Q24 comp forecast to -2.0% from -1.5%. We are also tweaking down LOW 1Q SSS forecast to -5.5% and don’t expect LOW to change the guidance outside of the potential impact from the pending late fee decision.

Although we recognise sentiment may be negative on the LCCs until we get some clarity, on balance we would buy Ryanair/easyJet on the share price weakness. Our actual estimate changes for Ryanair are minimal, and with our modelled fares up <1% for Mar-25E, there could be room for earnings upgrades as the year develops, and with an unchanged structural growth story and potential share buyback to be announced this year. Our ratings are unchanged; OW Ryanair, OW easyJet, N Wizz.

While data centers have been scrutinized for heavy electricity use, the water intensive nature of their operations has been comparatively overlooked. Building on our work on water as a sustainable investment theme, we deep dive into data centers, providing a comprehensive 101 on where, why, and how water is consumed. We also provide an overview of low water use heat rejection technology, and efficiency options, that can alleviate the water burden that AI likely brings.