This document is being provided for the exclusive use of lupin@bank.gov.ua.

20 December 2024

US Natural Gas

January price gets its wings

* This will be the last US Natural Gas note of the year. We want to thank all of our readers for another spectacular year of ups and downs in the US natural gas market and look forward to continuing the conversation in the new year. Happy Holidays!!

Largely driven by the potential for increased cold in January, the prompt futures contract finds itself higher than where it started the month, now comfortably above $3.60/MMBtu at the time this publication was penned. We believe that the moves higher at the front of the forward curve this week are likely the result of unwinds of residual bearish positioning while also new allocation of length is likely being entertained. This length is supported by three structural risk factors that continue to lend to increased tightness in the supply and demand balance: 1) fairly robust natural gas power burns, 2) a strong starting ramp higher in feedgas flows to Plaquemines, and 3) production continuing to underperform our expectations.

We caution that weather will be the most important risk factor to watch, and if weather were to turn warmer, much of the premium that has been embedded in the market will likely drain out. But with structural tightness from both supply and demand underpinning the balance, any colder additions to weather – particularly in the eastern half of the country – will likely elicit outsized moves higher in price. This is particularly true since the market – including ourselves – are unsure as to how quickly production can respond and at what price point we could actually see gas-to-coal switching in a meaningful way to alleviate any increase in weather demand.

As a final point, we would encourage our readers to watch Henry Hub cash pricing in January. If weather is to perform in the South Central region, an increase in feedgas flows to Plaquemines could continue to manifest just as a major pipeline network – NGPL – is expected to undergo maintenance from January 3 to January 17, potentially reducing flows headed toward Henry Hub. Over the past several months, Henry Hub cash rallies – which have elicited Nymex-related rallies – have ensued as maintenance on this pipeline network has occurred. We think this will offer the market glimpses of just how tight Henry Hub can get in 1H25 as Plaquemines continues to ramp higher in feedgas flows.

Based on revisions to our balance that we describe below, our current end-October storage trajectory points to 3.98 Tcf with the reduction in the current month’s weather demand. That said, we think there are plenty of opportunities between now and the end of winter to see that end-October storage trajectory move significantly in either direction – lending to what we believe will be increased volatility in price during summer 2025.

December weather retreats to the 10-year normal

At the start of the month, December weather forecasts indicated that the month would realize more than 1-standard deviation colder than the 10-year normal; however, that was not meant to be. Today, weather forecasts from CWG indicate that the lower-48 will likely realize 775 heating degree days, which is just shy of the 10-year normal. The retreat in weather forecasts has been due to increased warming in the eastern half of the country, but, of late, blocking of that warmth has the potential of reforming, suggesting that increasing cold could be in the cards for January. CWG has introduced more cold to its January weather forecast, now 900 HDDs – 3 HDDs warmer than the 10-year normal.

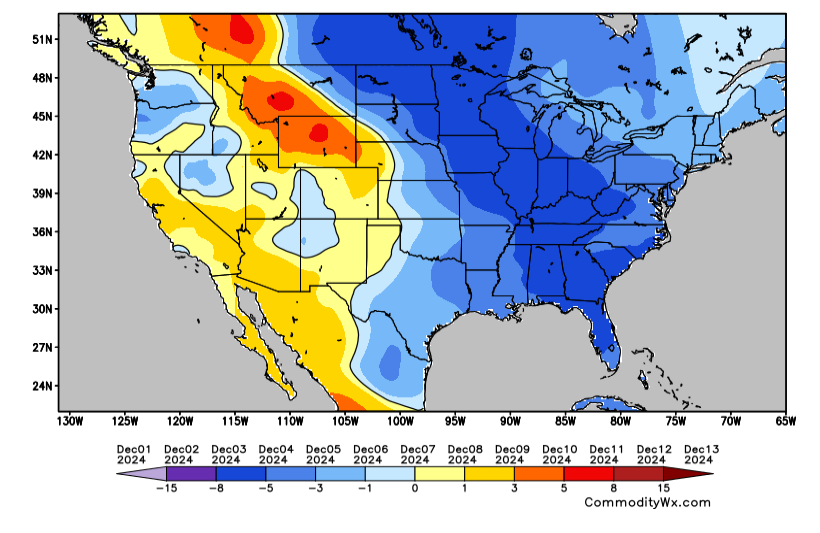

Figure 1: Surface temperature anomaly vs 10-year normal – Dec 1-13

Fahrenheit

Note: December 1-13

Source: CommodityWx.com, CWG

December power generation outperforms our expectations

Despite weather now expected to come in near the 10-year normal, we find that power burns have continued to outperform our expectations. During the first 13 days of the month, EIA 930 data suggest that natural gas–fired power generation has likely outperformed our monthly average expectation by as much as 3.7 Bcf/day. This is likely to do with the cold start to the month experienced in the eastern half of the country (see Figure 1).

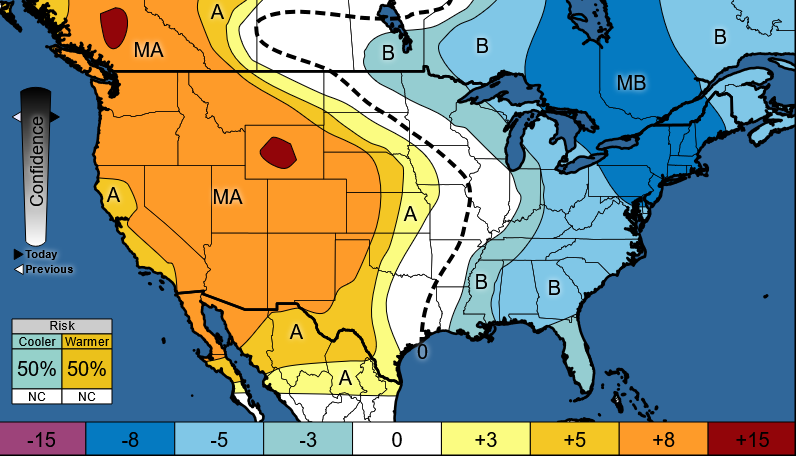

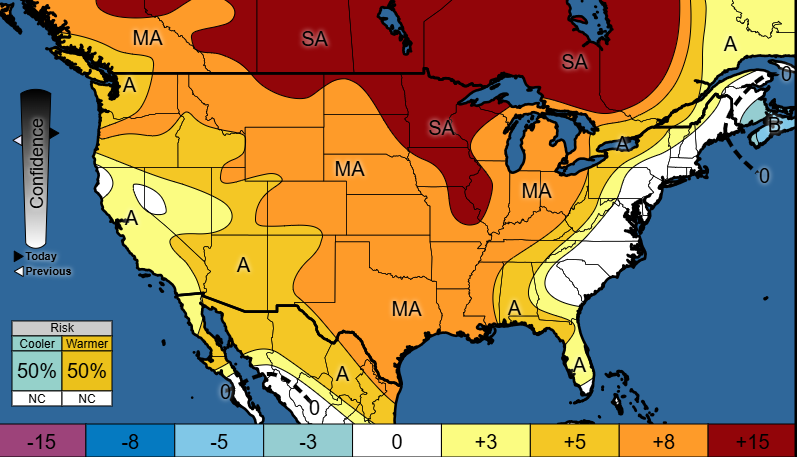

Despite the expectation of warmer weather in the 6-10 day period (Figure 3), in the near term, another bout of cold is anticipated to cover much of the eastern half of the United States (Figure 2). This near-term cold blast is likely to bolster heating-related power generation demand, suggesting that despite warmth anticipated in the offing, our power generation estimate for December is likely too low at 33 Bcf/day. Therefore, we have revised our December natural gas power burn level higher by 700 MMcf/day since our last publication, now at 33.7 Bcf/day.

We would point out that this underestimation has been a consistent theme with our US natural gas balance. And as we look forward to the remaining peak months of winter, we continue to believe that our model is reflecting a benign power burn profile. With January weather that is anticipated to be close to last year’s weather for the lower 48 states and with a regional breakdown that suggests increased cold in the East and Midwest yoy, we believe it is necessary to raise our January natural gas power burn average by at least 1.5 Bcf/day to 33.7 Bcf/day – flat to December.

Price will play an important role going forward in any gas-to-coal switching that could present. While it is still too early for us to triangulate, we are noticing that the first half of the month resulted in a sizeable increase in coal-fired power generation. Coal-fired power generation is currently accounting for more than 18% of the power stack, owing to the increased weather-related demand during the first half of the month, versus November, when it was ~15% of the stack, and last year when it was 17% of the stack. Notably, December 2023 weather was significantly warmer than normal. We do believe that at current price levels some switchback to coal should occur, but we are the first to admit that we are in the dark as to how much of much switching can actually manifest. While in 2024 there were limited coal-fired plant retirements – with ~1.9 GW retired through September and another 420 MW expected to be retired this month according to EIA-860 data – that data also suggest that another ~11 GW could be retired next year. This large amount of retirements could potentially make switching that much more difficult to achieve. For us this suggests far more volatility for natural gas price, particularly this summer, with those switching price levels largely unknown to market participants.

Figure 2: 1-5 day forecast – as of December 19th

Source: CWG

Figure 3: 6-10 day forecast – as of December 19th

Source: CWG

Plaquemines achieves first liquefaction

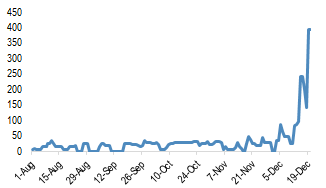

Alongside strength in natural gas burns, the operator of Plaquemines announced last weekend that its facility had achieved first liquefaction. Since then, feedgas flows to Plaquemines have increased to nearly 400 MMcf/day, suggesting enough gas for at least four trains. We currently have January feedgas for Plaquemines averaging 350 MMcf/day, which is clearly starting to look too low. We will refrain from adjusting our Plaquemines higher just yet,but continue to caution to our readers that there is a potential for its increase in feedgas flows to outpace market expectations with flows having the potential of surpassing 1 Bcf/day by the end of January. We are now at the mercy of the mechanics of the facility and will watch the ramp closely. Though, we do believe risks are mounting to adjusting our feedgas flows to the facility higher in January and beyond.

Figure 4: Plaquemines LNG Feedgas Flows

MMcf/day

Source: Bloomberg Finance L.P., J.P. Morgan Commodities Research

In addition to Plaquemines taking more feedgas, Corpus Christi’s expansion appears to be also progressing closer to first liquefaction. The facility received permission by FERC to introduce cold nitrogen gas into the LNG rundown line. We estimate that by the end of 1Q25 the expansion will likely result in additional 150-200 MMcf/day of feedgas flowing to the facility.

Production continues to underperform our expectations

While we were expecting production to average 105 Bcf/day this month, so far Wood Mackenzie/Springrock daily production prints suggest that production is actually averaging nearly 1 Bcf/day lower. While production is performing relative to our expectations in the three key gas producing regions of the Northeast, Haynesville, and Permian, a further push of production that was anticipated at higher prices at this time of year in other regions has not yet manifested. From the daily production data, we can see some increases in production from the Mid-continent – rising nearly 200 MMcf/day on average from October. But beyond this push in production and the already manifested push higher in Northeast production to meet seasonal demand, the question becomes where will more production come from if colder-than-normal weather presents.

We have long been hearing about turn-in-lines (TILs) and drilled, but uncompleted (DUCs) wells that are likely to come on line to respond to increased demand and higher price in 2025. However, we do believe that there is a mismatch in timing that could present between demand and the appearance of that supply. As one producer has already highlighted, there is at least 1 Bcf/day of spare capacity of new production through TILs and DUCs that can come on line in 2025. And we absolutely believe that this production and then some is there; but the question remains, if weather presents in January, can that production manifest fast enough to make market participants comfortable enough to stand in front of the type of price rallies that have realized this past week? We think that it will be difficult to see a significant amount of production to react to the potential for an outsized increase in weather-related demand. Ultimately, we believe that spare capacity in production is likely nearly tapped in the near term. Rather, the market will have to incentivize new production to come on line through sustained higher prices.

We think that alongside the demand portion of the balance beginning to structurally perform (through increased LNG feedgas and robust natural gas power burn), the lack of response from the supply side may be providing support for the robust strength in price this week amid the potential for weather in January to appear and alongside the cleanup of any residual bearish positioning. We continue to believe that summer 2025 production will struggle to breach significantly higher than 106 Bcf/day given the lack of increased drilling activity. That said, with enough of a price incentive early in 2025, we do believe that production can grow to nearly 108 Bcf/day by the end of the year – a necessary feat with the anticipated growth from LNG feedgas demand expected this year.

Figure 5: J.P. Morgan Commodities Nymex NG price forecast

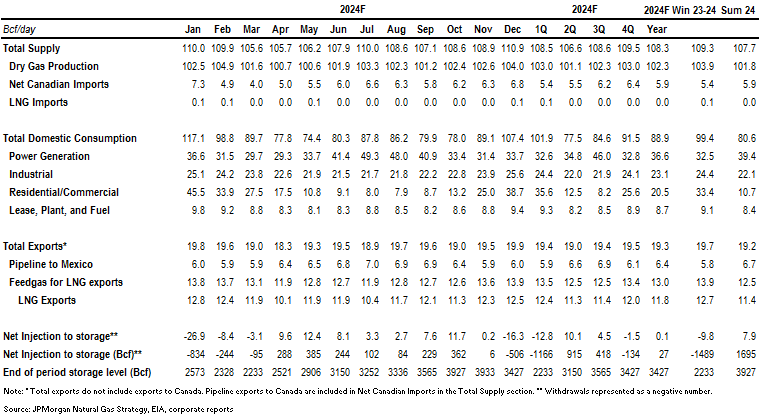

Figure 6: J.P. Morgan Commodities 2024 Lower 48 natural gas balance

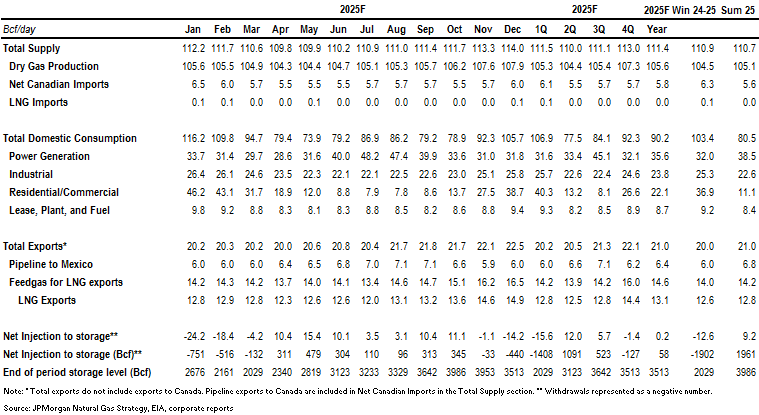

Figure 7: J.P. Morgan Commodities 2025 Lower 48 natural gas balance

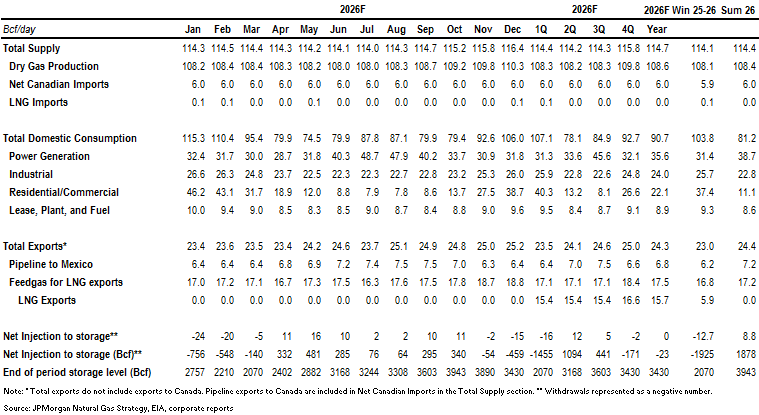

Figure 8: J.P. Morgan Commodities 2026 Lower 48 natural gas balance