The J.P. Morgan View : Megacap rally masks ‘high for long’ worries

This document is being provided for the exclusive use of blake@sandboxfp.com.

01 May 2024

The J.P. Morgan View

Megacap rally masks ‘high for long’ worries

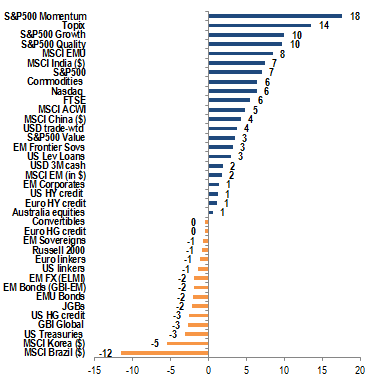

YTD returns by asset

Source: J.P. Morgan.

Cross-Asset Strategy: While Q1 earnings remain in focus this week, beyond this we remain concerned about the repeat of last summer’s drawdown, where the Growth-Policy tradeoff could move away from the Goldilocks narrative, together with a continued risk of concentration reversal, too steep projections for earnings acceleration this year, and positioning unwind. The strong momentum in consumer spending prompted our economists to revise up 2Q24 US growth to a 2.5%ar from 1.5%. Ahead of the FOMC meeting, we see Powell’s opening remarks echoing recent comments that 1Q24 data haven’t increased its confidence of getting back to its 2% target, so we stay neutral on outright duration and prefer 5s/30s steepeners. In the Euro area, stronger than expected domestic data contributed to the sell-off, though our economists expect the April inflation print to show continued disinflation, so we prefer duration proxies such as curve steepeners in 10s/15s Germany and 2Yx2Y/10Yx10Y EUR. Despite broader market volatility, US HG spreads are still near YTD tights and are modestly tighter on the month, as the resilient underlying technicals within HG are limiting its consequences to spreads. In Euro HY, we remain unenthusiastic about valuations, but with the strong technical only easing modestly, we lower our spread target. The USD’s bull run is consolidating. Concerns around the outsized jump in USD positions are valid, but the latter is loose as a contrarian USD signal, so we focus on the maturation of the monetary divergence narrative in US-RoW forward rate pricing. Commodities are not a deflationary force anymore; commodities represented ⅔ of the drop in the US headline CPI inflation from its 2022 peak, but that trend is reversing as the broad commodity complex rebounded and the rally may have another 10%+ to run.

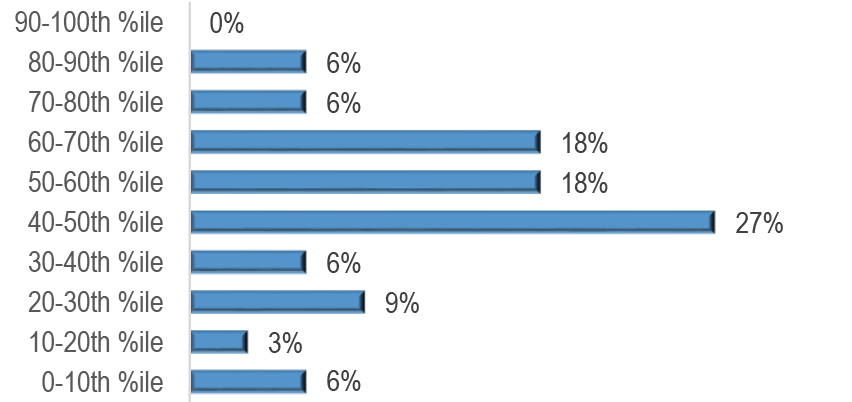

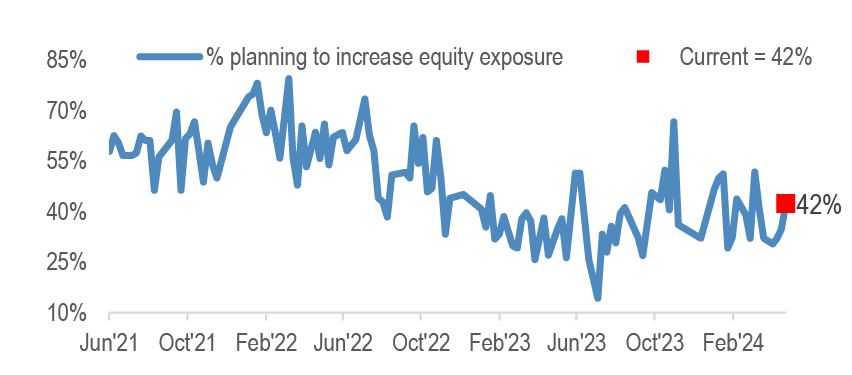

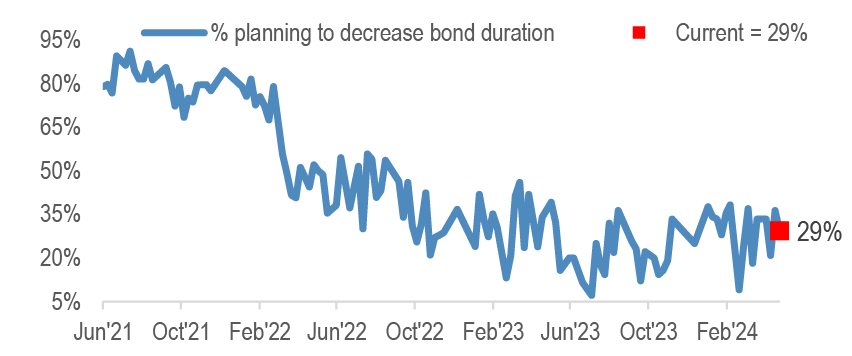

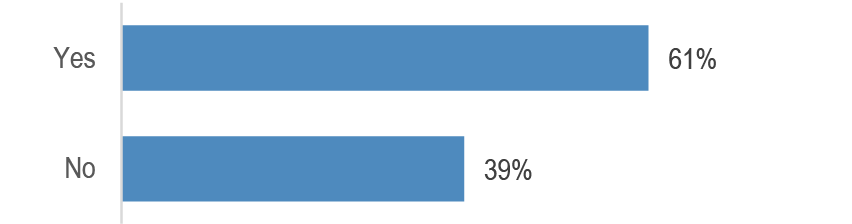

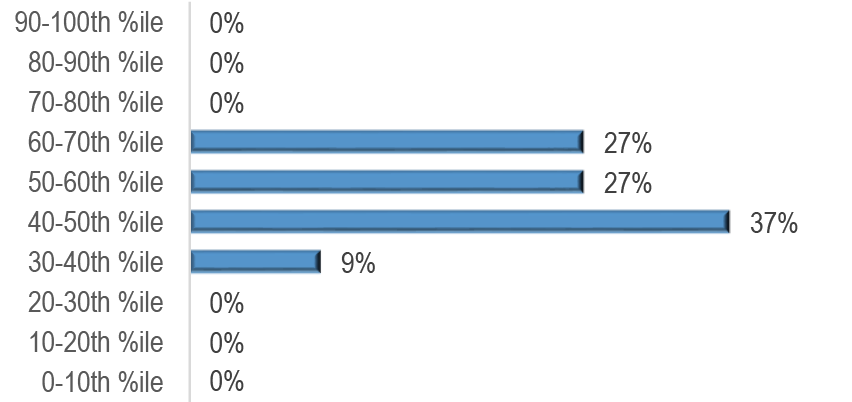

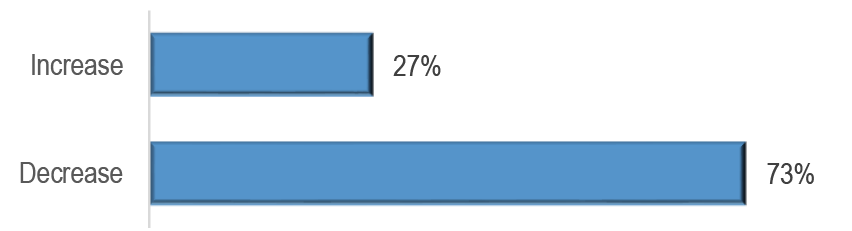

JPM Clients’ View: Click here to take this week’s survey. This week we poll investors on USD, Q1 earnings and the BoJ, in addition to our running sentiment questions. Our last survey results indicated: (1) equity exposure/sentiment among respondents is ~49th percentile on average; (2) 42% planned to increase equity exposure, and 71% to increase bond duration near term; (3) most respondents believe the recent correction isn’t over and look for a drawdown of 10%, and on average they expect the VIX to trade around 18 over the rest of Q2; (4) 47% believe Fed hawkishness will be a drag for EM; (5) 61% expected the BoJ to intervene in the Yen within the next few months.

Megacap rally masks ‘high for long’ worries: The downside surprise on US Q1 GDP and upside surprises on inflation send a negative message that is pressuring the ‘soft landing’ narrative and continues to point to ‘high for long’ risks. While the worry for risk markets is overheating that jeopardizes rate cutting, the recent GDP print heads in a stagflationary direction relative to market expectations.

Upcoming Catalysts: China PMI (4/29); Euro CPI, Q1 GDP (4/30); FOMC, US Mfg PMI/ISM, ADP report, BoJ March minutes (5/1); US Durable Goods/Trade Balance, Euro Mfg PMI (5/2); US Payrolls, services PMI/ISM (5/3).

Cross-Asset Strategy

Economics

Despite US 1Q shortfall, raising DM GDP growth forecasts as US consumers and Europe surveys impress. Slower government spending growth and a rise in consumer energy prices contributed to a slowing in US growth last quarter but GDP details show the US expansion stands on strong footing and will remain a positive for global demand. A net trade drag related to a rebound in imports is a key contributor to the 1Q24 moderation. However, domestic final sales have been tracking a steady 3%ar gain in recent quarters, and the US consumer shook off large income drags from rising taxes and inflation last quarter as the household saving rate fell further. Rather than a source of concern, we view this fall as a reflection of healthy fundamentals as both wealth and labor income are rising at a strong pace. Accordingly, our US team raised its forecast for current quarter GDP growth to 2.5%ar.

Anticipation that a broadening in global growth would be accompanied by sticky inflation is the key to our high-for-long rates narrative, and there is now strong evidence that the global disinflation process has stalled. A US gap between core CPI and PCE inflation closed with both baskets rising at about a 4.5%ar in the first three months of the year. The Euro area saw a similar rebound in core inflation to a 3.8%ar. The early year inflation spike likely overstates its underlying trend, and we look for global core CPI to moderate to a 3.1%ar this quarter. Much of this slide should be concentrated in the DM economies.

BoJ signals it will remain gradual amid sluggish recovery. In last week’s BoJ policy meeting, Governor Ueda delivered dovish guidance. The BoJ adjusted its inflation forecasts to around 2% across all forecast periods and added some ambiguity in its guidance on JGB purchases, but did not commit to any immediate reduction to the pace of buying. We draw two messages from the meeting: 1) the BoJ will remain committed to gradualism as long as Japan’s macroeconomic outlook remains uncertain; 2) by downplaying the importance of the Bank’s commitment to maintaining the “current pace” of JGB purchases, we think the BoJ has introduced further flexibility into its balance sheet policy. We continue to think that the pace of future purchases will decelerate (GDW, Apr 26th).

Equities

Eurozone delivering on an improving risk-reward. At the overall market level, we remain concerned about the repeat of last summer’s drawdown, where the Growth-Policy tradeoff could move away from the Goldilocks narrative, together with a continued risk of concentration reversal, too steep projections for earnings acceleration this year, and position unwind. We don’t expect Eurozone to directionally decouple from the US, but we see an improved relative risk-reward for Eurozone equities versus the US due to: 1) The sector neutral P/E discount is near the largest pre COVID. Total equity yield vs bond yield is much more attractive in Eurozone than in the US. 2) ECB is set to start cutting ahead of the Fed, and by a greater magnitude, and PMI momentum is improving in Eurozone vs the US. 3) Tactically better China performance will help Eurozone vs the US trade. 4) The risk of extreme concentration and momentum unwind is much bigger in the US. Notably, small caps begin to perform better post the start of ECB cuts ( Equity Strategy , Apr 28 th ).

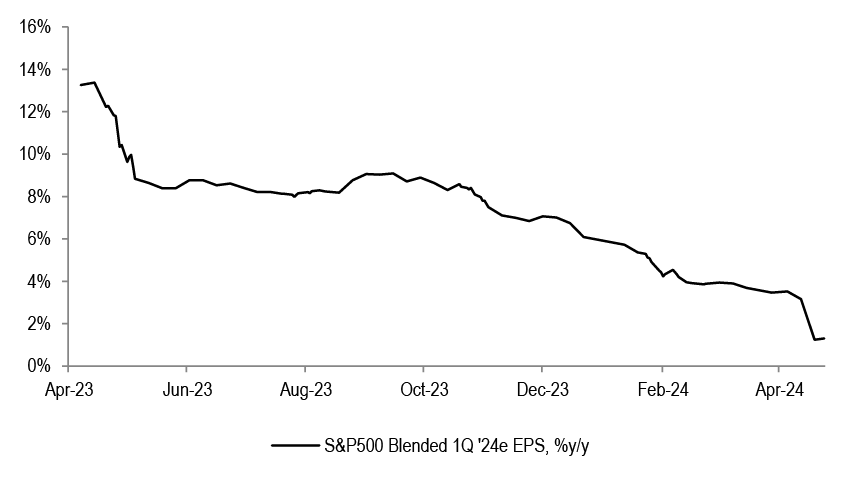

We are in the busiest weeks of the Q1 reporting season, with a third of companies having reported in both the US and in Europe, so far. S&P 500 Q1 ’24 blended EPS projections were cut by an additional 3% in the last month, and are not showing signs of a customary inflection higher as yet. This feeds into our concern that earnings estimates for this year are likely too high, and are at risk of further downgrades. 79% of S&P 500 companies that have reported beat EPS estimates. EPS growth for these companies is at +6% y/y, surprising positively by 8%. Top-line growth is printing at +3% y/y, surprising positively by 1% (Equity Strategy, Apr 25th).

We have come up with our Japan Core 30 Basket that we expect to outperform the market over the next 5-10 years. Japanese stocks have room to rise thanks to structural changes, but we think the market is in a stock selection phase. Using a bottom-up approach, we selected promising, future-oriented stocks in sectors where Japan has advantages and are plays on such themes as semiconductors and AI, automation and labor saving, digital, and decarbonization, which address such challenges as population decline (Japan Equity Strategy & Cross Sector, Apr 22nd).

Bonds

Bonds sold off again last week amid stronger than expected PMIs. In the US, the strong momentum in consumer spending prompted our economists to revise up 2Q24 growth to 2.5% annualized from 1.5%. Ahead of the FOMC meeting, we see Powell’s opening remarks echoing recent comments that 1Q24 data haven’t increased its confidence of getting back to its 2% target. While markets have priced out cuts and yields are trading cheap, we stay neutral on outright duration and prefer 5s/30s steepeners to position for eventual easing as well as higher term premia.

In the Euro area, stronger than expected domestic data contributed to the sell-off, though our economists expect the April inflation print to show continued disinflation. We retain a medium-term bullish view, but prefer proxies such as curve steepeners in 10s/15s Germany and 2Yx2Y/10Yx10Y EUR swaps and option structures such as Jun24 1Y Euribor midcurve call ladders. In the UK, yields are higher on a combination of MPC commentary and UK PMIs; we pare back bullish proxies and unwind Aug24/Nov24 MPC flatteners, but keep 1Y/1Yx1Y SONIA curve flatteners.

In EM, local yields now look cheap in much of Latam and EMEA EM after a sell-off, but risks remain binary ahead of coming CPI prints. As a result, we stay neutral local bond duration overall, with selective OWs via Brazil, Colombia, Uruguay, Czechia and Poland, offset by a short duration overlay and UW in Thailand (EM Fixed Income Focus, Apr 25th).

Credit

Despite broader market volatility, US HG spreads are still within 5bp of their YTD tight and are modestly tighter on the month. This is not to say HG has been completely immune to this volatility but thus far the resilient underlying technicals within HG are limiting its consequences to spreads. Namely, HG inflows have slowed significantly as rate vol has picked up and total return losses hover around -3% YTD, but on the flipside supply has also slowed significantly. In our view, there is good reason for HG to continue to outperform on a relative basis against a ‘higher for longer’ backdrop. The key risk of course is if this shifts to a discussion of the possibility of further rate hikes instead. In this scenario, we think the still strong HG technicals would likely weaken significantly (CMOS, Apr 26th).

We remain unenthusiastic about valuations, but with the strong technical only easing modestly, we lower our Euro HY spread target to 400bp. Euro HY credit spreads excluding the widest 10% of bonds have compressed below 300bp, a level that has rarely been breached since the GFC (European Credit Weekly, Apr 26th). European HY issuer net debt / EBITDA fell by 0.2x to 4.5x over 4Q23, reversing the first-half bounce in leverage. Adjusting for composition effects, earnings delivery was soft. Revenues and EBITDA declined 5% and 3%, and net debt increased 1.4% y/y, although gross debt fell by 0.5%. Interest coverage continued to moderate, dropping 0.25x in 4Q23 to 5.4x, with BBs seeing the fastest improvement (HY Talking Points, Apr 23rd).

Currencies

Grappling with a mature USD uptrend. The USD’s bull run is consolidating after a 3% surge since early March. Concerns around the outsized jump in IMM USD positions are valid, but the latter is loose as a contrarian USD signal. Of greater import, in our view, is the maturation of the monetary divergence narrative in US-RoW forward rate pricing. The neutralization of stark early ’24 asymmetry in USD rates/FX valuations and positioning is also running into a pivotal period of US dataflow that carries almost binary risks for the Fed cycle this year, leading us to tactically trim USD length. A dovish BOJ hold puts paid to hopes of a monetary policy short-circuit for Yen weakness, but intervention threat is likely to render USD/JPY buying a noisy proposition.

Trade Recommendations:Reduce USD longs via USD/CHF cash, but keep USD/CHF call spread. Enter NOK/SEK cash longs. Take-profit-stop hit in long SEK/CZK cash. Hold USD longs vs GBP, CAD, CNH, EUR into the FOMC meeting. Keep CHF/JPY digital put. Stay MW EM FX (FXMW, Apr 26th).

Commodities

Commodities are not a deflationary force any more. Commodities were responsible for ⅔ of the drop in the US headline CPI inflation from a peak of 9.1% in June 2022 to 3.4% in December 2023. In this sizeable 570bp fall in inflation, oil alone contributed a 300bp decline, with drop in agricultural prices delivering another 100bp. In a reversal of the trend, and directionally in line with our view, the broad commodity complex is up 8% from February lows and the rally may have another 10%+ to run. Our top 3 buy recommendations, in order: US HH natural gas, copper, and gold. Our base case on oil is unchanged, with a bullish risk bias. Six powerful structural shifts are likely behind the unfolding rally: 1) return of industrial policies, 2) rise of strategic stockpiling, 3) de-dollarization and the shift in gold’s ownership base, 4) race to secure 34 critical minerals, 5) AI demand for energy and metals, and 6) populism and breakdown in the theoretical project incentive model in copper (Global Commodities, Apr 25th).

Nearly all clients at CESCO Copper Week were structurally bullish copper over the medium-term, though near-term, there was still a sense that the current copper rally may be running ahead of the fundamental story. Chinese demand has clearly been dented by higher prices for now but most participants did not view it as symptomatic of a broader miscalculation on underlying Chinese end use, but rather a more temporary pause in purchasing with demand eventually acclimatizing to higher price levels. By 2028, we currently see a need for an additional 1.4 mmt of new copper supply. Last year, new project sanctions amounted to a measly ~350 kmt. Given the lead time necessary to even bring on more incremental capacity, we think we are in a critical window where time is running out to get projects going to avoid a serious shortfall in supply. Our view, which we sensed was in the back of many producers’ minds, is that in the absence of a stronger supply response, copper prices will search higher for a level where enough demand is destroyed in order to rebalance the market. In our current thinking, a price level around $14,000-15,000/mt likely incentivizes more significant substitution and accelerates copper intensity thrifting (Metals Weekly, Apr 24th).

This week, we poll investors on USD, Q1 earnings and the BoJ, in addition to our running survey questions on equity positioning/sentiment, and intentions for near-term changes to equity allocation and bond duration. The results from the last survey are shown below.1

Figure 1: What is your current equity positioning or sentiment in historical terms, expressed from most bearish (0th percentile) to most bullish (100th percentile)?

Source: J.P.Morgan

Figure 2: Are you more likely to increase or decrease equity exposure over the coming days/weeks?

Source: J.P. Morgan.

Figure 3: Are you more likely to increase or decrease bond portfolio duration over the coming days/weeks?

Source: J.P. Morgan.

Figure 4: Is the recent correction in risk assets likely to continue and, if so, how large of a drawdown do you ultimately expect on the S&P 500?

Source: J.P. Morgan.

Figure 5: What do you expect the VIX to average over the rest of Q2?

Source: J.P. Morgan.

Figure 6: Do you believe Fed hawkishness will cause a material growth drag in Emerging Markets?

Source: J.P. Morgan.

Figure 7: Do you expect Japan to intervene to support the Yen within the next few months?

Source: J.P. Morgan.

JPM Clients’ View - This Week’s Interim Survey Results

The charts below show interim results from this week’s survey, collected over the first ~24 hours it was live. The survey remains open here, and we will show updated results in the next J.P. Morgan View publication

Figure 8: What is your current equity positioning or sentiment in historical terms, expressed from most bearish (0th percentile) to most bullish (100th percentile)?

Source: J.P.Morgan

Figure 9: Are you more likely to increase or decrease equity exposure over the coming days/weeks?

Source: J.P. Morgan.

Figure 10: Are you more likely to increase or decrease bond portfolio duration over the coming days/weeks?

Source: J.P. Morgan.

Figure 11: What do you expect the US dollar to do over the next 2-3 months?

Source: J.P. Morgan.

Figure 12: Do you believe dollar strength will be a headwind for risk assets this year?

Source: J.P. Morgan.

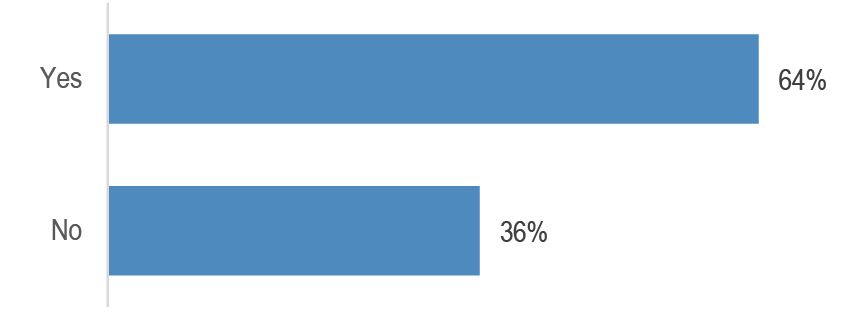

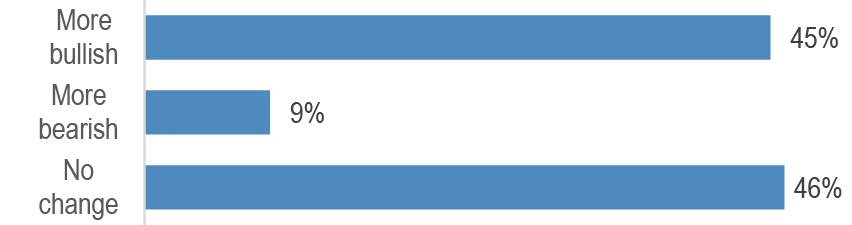

Figure 13: Have Q1 earnings announced so far made you more bullish or bearish on equities?

Source: J.P. Morgan.

Figure 14: When do you expect the BoJ will meaningfully reduce rinban purchases?

Source: J.P. Morgan.

Megacap rally masks ‘high for long’ worries

After the stock pullback in 1st half of April, efforts to stage a comeback seem to be stalling, with the recent GDP reading sending a message that was not well-received by the markets. If the hot prints YTD on growth and inflation have created worries about ‘high for long’, the hope for the ‘soft landing’ camp was that the disinflation would reassert itself, as the troublesome inflation components would settle down. In particular, rent inflation could head lower based on where the Zillow rent index is, and auto insurance can calm down on the assumption that additional upticks in insurance premiums would moderate, having largely caught up to the increase in claims post-COVID. So while the worry for risk markets is overheating that jeopardizes rate cutting, the recent GDP print, introduces a new worry, as US GDP grew 1.6% q/q saar in the first quarter of this year, significantly disappointing consensus expectations for a 2.5%ar gain and our own tracking of 2.3%ar. Meanwhile, the core PCE price index rose 3.7%ar in 1Q, which was notably firmer than the 2.0%ar pace of the prior two quarters. So, in contrast to the overheating story, this print heads into a stagflationary direction relative to market expectations. Our economists revised their 2Q estimates for US real GDP growth to 2.5% saar, up from 1.5%, so we continue to emphasize the associated ‘high for long’ risks.

In Japan, the BoJ meeting produced no surprise. The BoJ decided to keep its policy rate unchanged at around 0-0.1%, while continuing asset purchases “in accordance with the decisions made at the March meeting”. At the March meeting, the BoJ stated that the bank would continue its JGB purchases “with broadly the same amount as before” and added in the footnote that “the amount of JGB purchases is currently about 6 trillion yen per month” as reference. Although the BoJ didn’t make a clear decision to reduce its JGB purchases, we believe this introduced some flexibility to the BoJ’s JGB purchases. Friday’s decision was broadly in line with our expectation. Currency markets found the BoJ outcome to be underwhelming, with USD/JPY rallying from ~155 to 157. Assuming the US exceptionalism continues, the direction of US yields should be the dominant force for USD/JPY, despite the looming threat of potential MoF intervention. Upside risks remain for USD/JPY since domestic JPY selling pressure is unlikely to wane so long as BoJ remains behind the curve ( Figure 15).

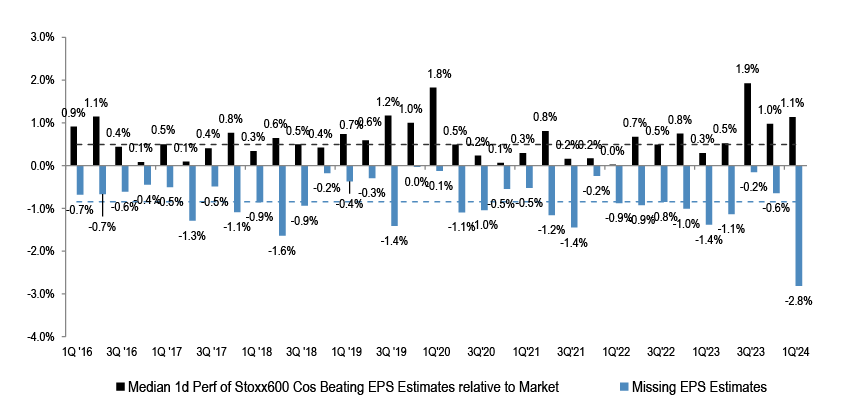

So far, we are not overly impressed with the earnings season. With ~42% of S&P 500 companies having reported, 75% are beating EPS estimates (vs. 73% average over the last 4Qs) by an average of 1.7%, while only 59% are beating revenue estimates (vs. 63% average) by an average of 0.5%. Additionally, the positive EPS surprise needs to be viewed in the context of the substantial downgrades to the S&P 500 blended Q1’24e EPS growth over the last few months ( Figure 16). Of the Stoxx600 companies that have reported so far, 54% beat EPS estimates. Q1 EPS growth is at -8% y/y, surprising positively by 2%. In Japan, 59% of Topix companies beat EPS estimates, with overall EPS growth at +1% y/y. Given the global stock rally leading up to the earnings season and the already stretched positioning, we believe stock reactions to the earnings season will continue to be underwhelming, with beats rewarded less, and misses penalized by more than usual ( Figure 17). In Europe, the sales beats are anemic relative to the history at 43%, and the reaction function for EPS misses is dramatically worse than we’ve seen in years ( Figure 18).

We continue to be UW Equities on the assumption that yields have finally reached a level where they are problematic. Equities looked the other way and produced a great Sharpe ratio from October to March, despite an 80bp uptick in yields. The combination of a hot CPI print and shift in the Fed’s tone upended the ‘bad news is good news’ narrative of 2024, as multiple strong CPI prints are no longer just ‘bumps in the road’. Given the April correction, we understand the temptation to play for a tactical bounce in equities, as technical signals like a high percentage of stocks at new lows suggest capitulation. In this case, the selling pressure could be exhausted and the time to the next print might allow for the soft landing / disinflation narrative to make a comeback, tempting some to ‘buy the dip’. However, allowing for further upside risk in yields, we can see a repeat of the mid-April correction so these tentative bottoming signals likely will not hold.

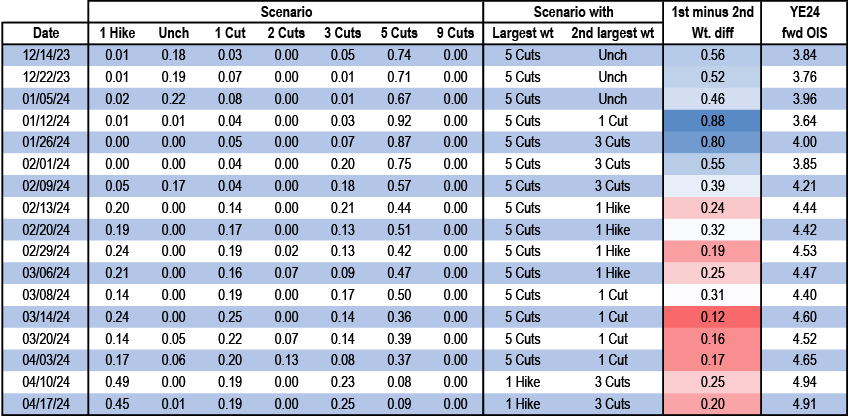

So, we would caution against buying the dip, as we are now facing two-sided risks on the rates path. The earlier conversation on the Fed trajectory during the soft landing narrative was relatively constrained, revolving around cuts coming a few months sooner or later. Despite rate cuts disappearing, we still seemed firmly in a world of more one-sided risk (how much cutting) and yield targets below the elevated levels after the bond correction of 2024. Now with only ~40bps of cuts priced to the end of the year, this modest amount of cutting is reflective not just of one dominant scenario, which had been for a long time 5 cuts, and now 1 hike indicates significant risk ( Figure 19). Our colleagues in Interest Rate Derivatives highlight this dramatic shift in regime as expressed in the options surface of December 2024 SOFR futures. The increase in policy uncertainty argues for a wider term premium. While our year-end target for the 10y is at 4.0%, the direction of travel for our yield targets and forecast revisions for growth and inflation has been positive. Digesting the incremental Treasury supply requires acceptable bond expected returns, and further upside risks to yields can bring us to the point where the price sensitive duration buyers demand more term premium for the new two-sided risks, and the higher yields likely will in turn choke equities.

If we can call the period from Fall ’22 a late-cycle meltup, one result of these periods would be a mediocre stock vs bond yield comparison and complacent risk. The stock vs bond risk premium comparison has tightened up due to the stock rally and ~500bps hiking from DM central backs. And the complacent risk environment was a reflection that growth risk had disappeared and that inflation was on a downward trend. In other words, the meager compensation from a tight risk premium is considered to be good enough in an environment where nothing is breaking. However, this tight risk premium likely is not sufficient when VIX leaves the comfortable channel between 13-15 it’s occupied since Fall 2023, and touches 19 as it did mid-April. We view this as a sign of things to come as complacency on ‘high for long’ goes away. Given a strong day on Friday and VIX coming down, are we back to complacency? Consider that just four stocks (GOOGL, NVDA, MSFT and AMZN) account for ~80% of this rally, putting the AI / megacap theme ahead of ‘high for long’ worries.

Figure 15: Japan is likely to stay behind the curve for another 2 years without BoJ’s commitment to rate hikes...

Source: J.P. Morgan Currency Research, BoJ, Bloomberg Finance L.P

Figure 16: S&P 500 blended Q1 ’24e EPS, %y/y

Source: J.P. Morgan Equity Research, Thomson Reuters

Figure 17: US stock price reaction* to quarterly EPS beats/misses

Figure 19: Policy Uncertainty ticks up as 1 Hike scenario gains prominence

Weights for conditional Normal distributions* that can be combined to create a composite distribution that recovers prices of SFRZ4 calls and puts at various strikes**, scenarios with largest weights, the weight differential between the two scenarios with the largest weights, and 12/31/2024x1M OIS rate (%), as of the dates shown

Source: J.P. Morgan., CME *1 hike scenario corresponds to mean of 5.5%, unchanged corresponds to a mean of 5.25%, 1 cut corresponds to mean of 5%, 2 cuts corresponds to mean of 4.75%, 3 cuts corresponds to mean of 4.5%, 5 cuts corresponds to mean of 4% and 9 cuts corresponds to mean of 3% **Implied distribution is assumed to take the form of a weighted sum of many individual Gaussian density functions with various different means and standard deviations. The weights are solved for by calibrating to the prices of 3M SOFR ATM and OTM calls and puts, while also recovering the SFRZ4 futures price

Investors have moved to a consensus around a high-for-longer soft landing, with a view that restrictive for longer will not morph into even higher for longer. Macro and geopolitical risks do not appear imminent, and the meetings were noteworthy for the sanguine tone and the greater acknowledgement on the positive role of fiscal policy in the global recovery. Inter-connectedness between the actors in private credit is a key risk to monitor, but demand is unlikely to abate. Top trade ideas include UW equities as there is a risk of a 5-10% pullback that would erase this year’s gains, OW cash with US rates at 5%, OW Commodities (gold and energy equally) and short Yen.

Investors remain sanguine about the market implications for the US elections, with only 12% of survey respondents at our conferences seeing US elections as the biggest threat to risk markets, far behind concerns on resurgent inflation (30%) and geopolitical turmoil. Survey respondents did not indicate a clear bias on who will assume the US presidency although 70% of investors expect a divided Congress to endure. Irrespective of a Biden or Trump victory, we expect greater use of industrial policy including strong support for the passage of a CHIPS 2.0 Act in 2025.

We do not think that P/Es can drive further equity upside without the support of earnings upgrades. Investors are expecting S&P 500 EPS to accelerate by almost 20% by Q4 compared to the projected Q1 ’24 levels. That hurdle rate is too steep in our opinion. We remain concerned about continued complacency in equity valuations, inflation staying too hot, further Fed repricing, rates moving higher for the “wrong reasons”, about profit outlook where the implied acceleration this year might end up too optimistic, high market concentration, as well as about the potential further escalation in geopolitical uncertainty.

Despite recent portfolio inflows foreign investors have become even more under-owned in Chinese onshore bonds compared to onshore equities. Different to the foreign ownership of Chinese onshore portfolio assets, the internationalisation of the Renminbi has re-accelerated in recent years, in part due to rising trade redenomination. This trade redenomination has been facilitated by the Belt and Road initiative, China’s growing role in energy and commodity trade as well as digital innovations in RMB-denominated trade finance and payments infrastructure.

Despite US mortgage rates having soared 295bp since the start of the Fed’s hiking cycle in 1Q22, US household debt servicing ratios have barely budged. As of 4Q23, the DSR remained below its pre-pandemic level. In this note, we show that the sluggish move in DSRs owes to three factors: extended duration and stable labor markets, a decade of leveraging, and nominal income gains ease the burden. The upshot is that even while debt servicing costs have risen, the impact has been more muted given healthy balance sheets and when looked at as a share of income.

We find limited evidence that long-run drivers of new business formation, namely population growth and import competition, changed drastically in the post-pandemic recovery. The recent surge in immigration, if it continues, could provide some boost for business formation, but secular forces are strongly in the opposite direction. Instead, we find plenty of evidence that this recent surge is related to a reshuffling of economic activity with a higher share of the workforce working from home. As the labor market finds its new equilibrium with a higher number of workers commuting less, the main impetus behind this newfound business dynamism will likely fade.

The risk of a renewed US-China tariff war is at the center of market focus and recent developments likely will accelerate the emergence of new trade corridors amid costly adjustment in global supply chains. US reliance on Chinese imports fell, benefiting ASEAN and Mexico. China lost US market share in ICT, critical minerals and energy products, but is still a key supplier in computer, smartphones, large-capacity batteries, nickel, and hydroxides. China increased ODI to ASEAN and Mexico to bypass tariff hikes and friendshoring constraint. A 60% universal tariff would accelerate supply chain relocation and disrupt trading patterns.

Although we still very much like gold as a structural multi-year bullish story with an updated price forecast of $2,600/oz, after two years at the top of the pecking order, from here, gold is replaced by US HH natural gas as our #1 buy recommendation. We believe no other commodity can match its return potential this year. Copper is our #2 buy recommendation. Gold’s structural bull case remains intact making it our #3 buy recommendation with a peak target of $2,600/oz. In this note, we highlight six powerful structural shifts that are likely behind the unfolding rally, along with an optimistic macro narrative.

We introduce a new report designed to highlight spread curve opportunities in the HG corporate bond market. The report identifies liquid bond pairs which are trading at the extremes of their usual trading ranges and also which have flattened/steepened the most WoW. It also details each liquid bond pair’s spread difference, where this difference stands in its 6m range and shows how steep/flat the pair is versus the overall curve. Lastly, it shows the relationship between sector curves and their spreads.

We have come up with our Japan Core 30 Basket that we expect to outperform the market over the next five to 10 years. Japanese stocks have room to rise thanks to structural changes, but we think the market is in a stock selection phase. Using a bottom-up approach, we selected promising, future-oriented stocks in sectors where Japan has advantages and are plays on such themes as semiconductors and AI, automation and labor saving, digital, and decarbonization, which address such challenges as population decline. Note: J.P. Morgan Research does not provide research coverage of this basket and investors should not expect continuous analysis or additional reports relating to it.

The EM corporate external bond asset class across corporates and quasi-sovereigns is $2.5tn in size, having exceeded the $1tn milestone reached in 2012 and $2tn in 2017. The current size of EM corporate external bonds is well above US HY ($1.3tn) and EM external sovereign bonds ($1.5tn). A frequently asked question is what we define as the EM external corporate bond asset class and how we apply the criteria in what to include or not. In this note, we go over our thought process behind such classification and explore the evolution.

The VRT print was a strong, upside result, highlighted by 60% orders growth and 62% incremental margins, well above the most bullish outlooks, and we come away raising our above-consensus estimates further, with increased conviction that these remain conservatively based. Management also noted accelerating demand on the back of a strong data center market, in which they remain uniquely well positioned to capitalize.

We undertake a First Principles deep dive of the global LNG value chain and assess key EU Majors producers on a five metric JPM LNG Scorecard. We highlight infrastructure limitations and price, LNG’s capacity to optimise margins against price/time spread fluctuations and LNG as a domain of the large-cap Majors.

The tanker shipping sector (both product and crude) looks set for an extended upcycle led by structural ton-mile demand growth and constrained supply growth.

Despite decent price performance YTD, the stocks are still at 0.9-1.7x FY24-25 average P/B (JPMe), which is undemanding and in our view does not fully price-in further tanker freight rate spikes driven by any further escalation of the Red Sea crisis and the Middle East situation.