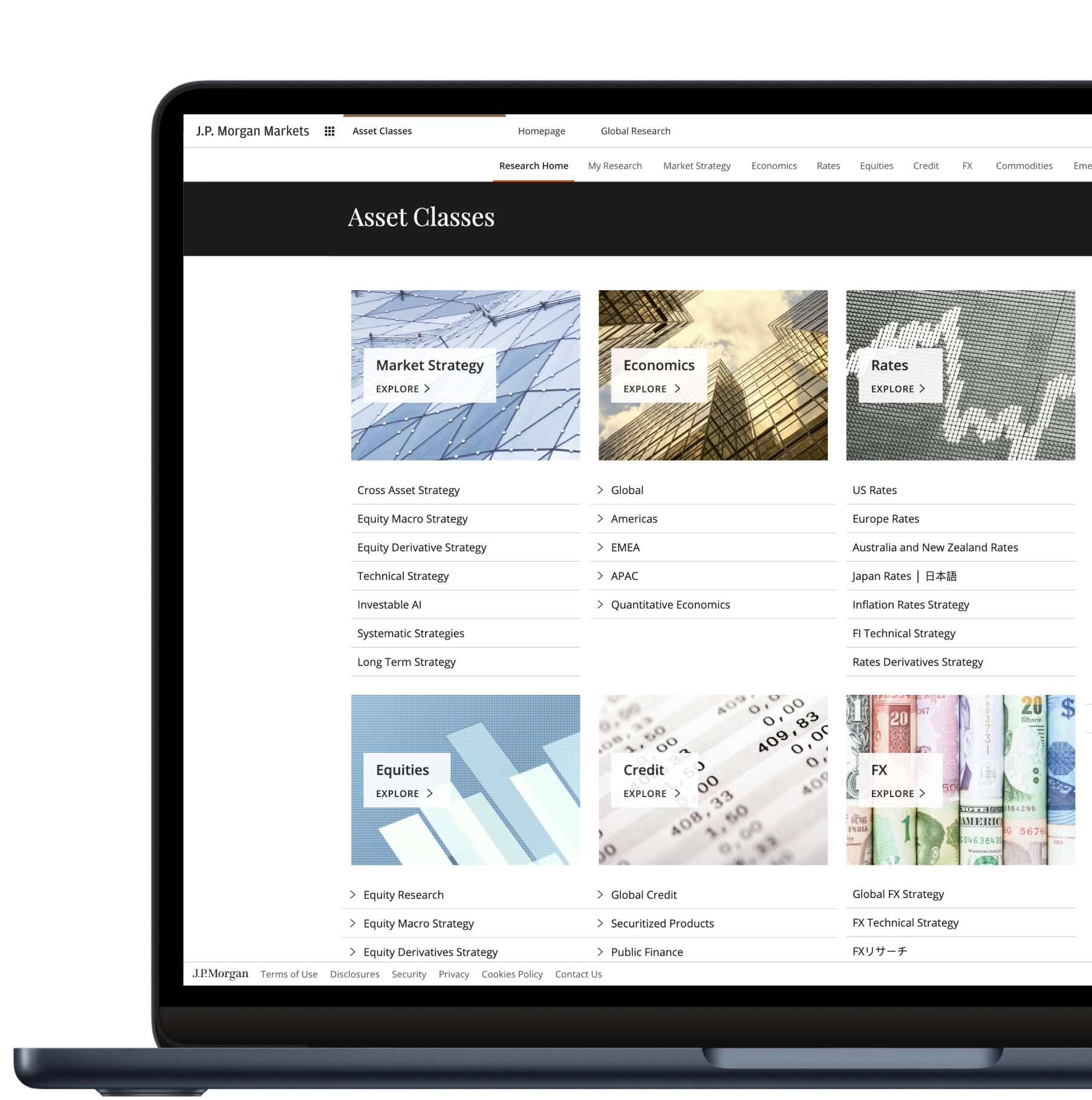

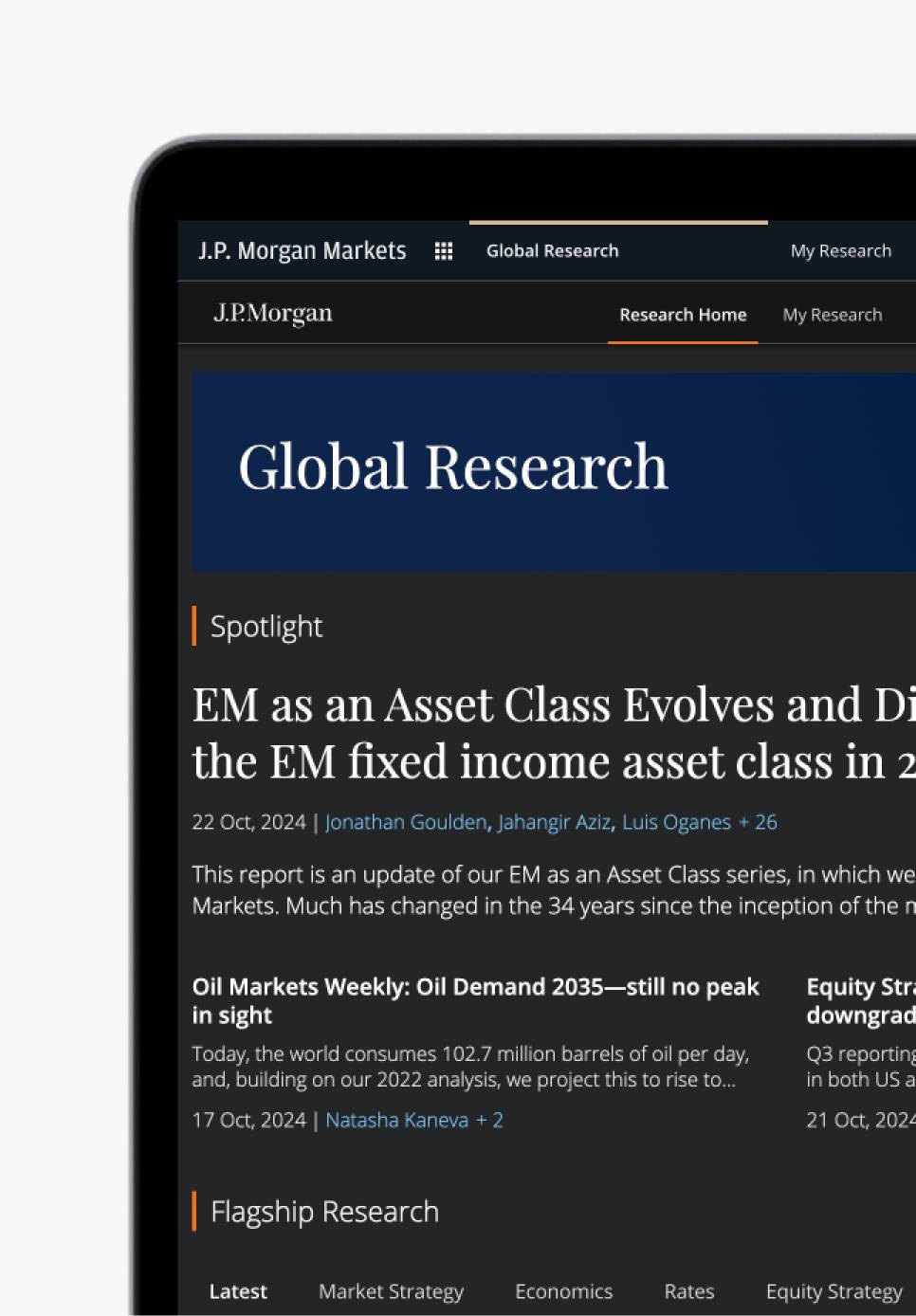

J.P. Morgan Research offers an extensive breadth and depth of independent coverage of more than 5,000 companies across sectors and asset classes in over 80 countries.

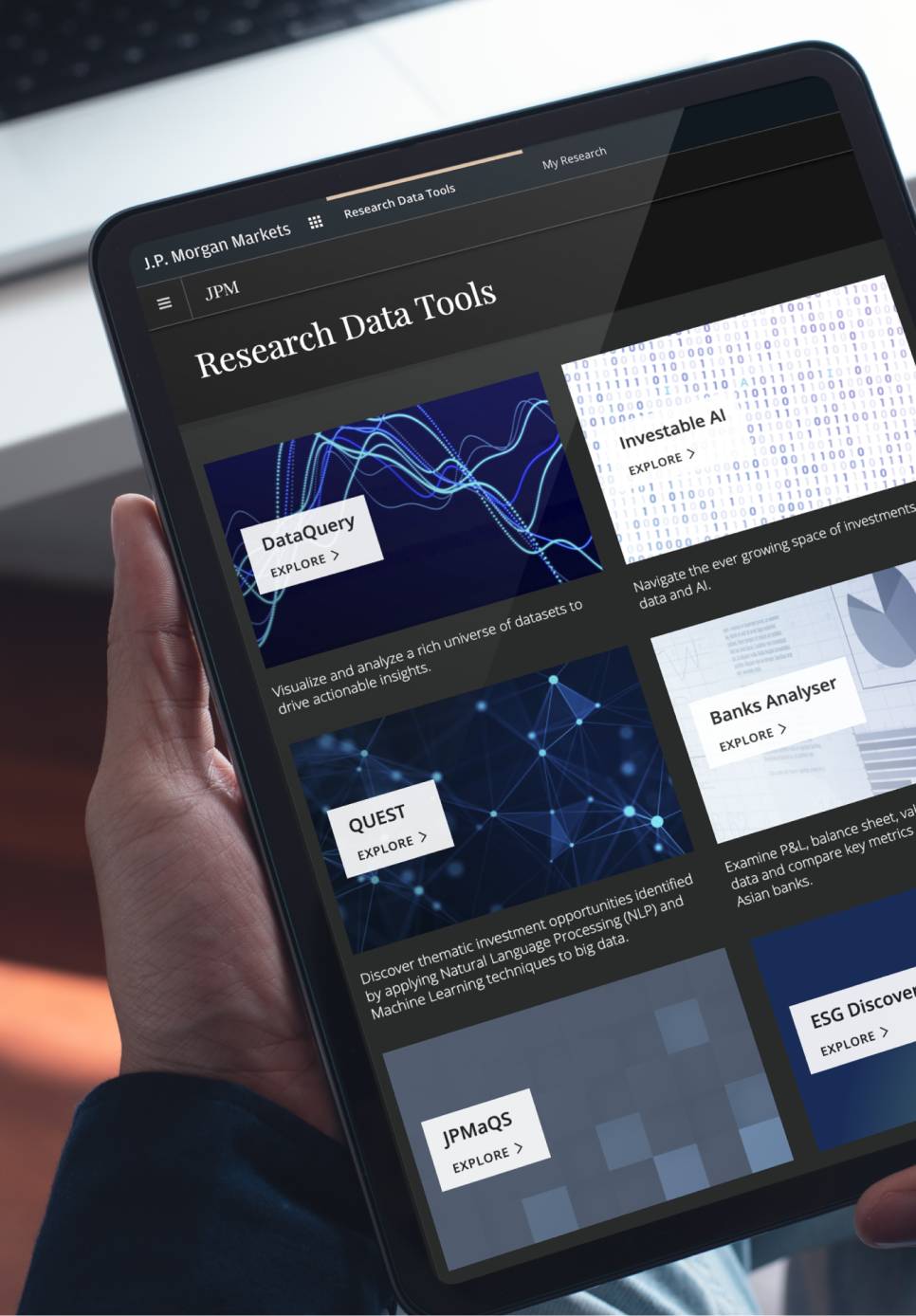

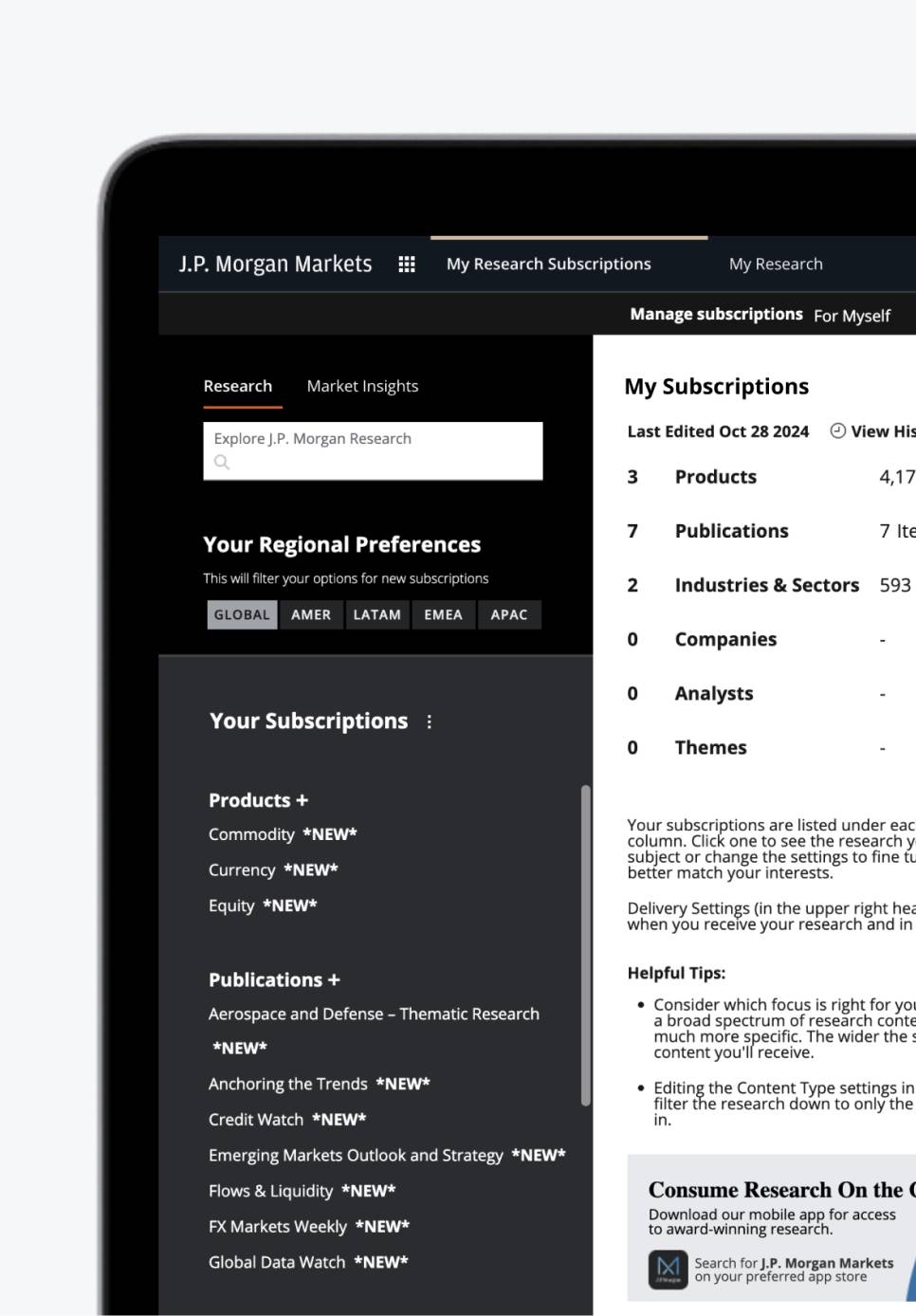

Our top-ranked teams produce market-leading research, including private company coverage and index research, accessible alongside innovative data and tools on J.P. Morgan Markets. Through our cross-disciplinary approach and expertise, we empower our clients with the actionable insights they need to make informed decisions anytime, anywhere